Can PMI be waived on FHA loan

If you bought a house with an FHA loan some years back, you may be eligible to cancel your FHA PMI today. … If your loan balance is 78% of your original purchase price, and you’ve been paying FHA PMI for 5 years, your lender or service must cancel your mortgage insurance today — by law.

When can I remove FHA PMI?

Getting rid of PMI is fairly straightforward: Once you accrue 20 percent equity in your home, either by making payments to reach that level or by increasing your home’s value, you can request to have PMI removed.

Can you refinance out of an FHA loan?

Refinancing your FHA loan to a conventional loan can be done and has a few benefits, including: Dropping your mortgage insurance. Lowering your interest rate.

How can I avoid paying PMI on an FHA loan?

One way to avoid paying PMI is to make a down payment that is equal to at least one-fifth of the purchase price of the home; in mortgage-speak, the mortgage’s loan-to-value (LTV) ratio is 80%. If your new home costs $180,000, for example, you would need to put down at least $36,000 to avoid paying PMI.How do you calculate if PMI can be removed?

Pay Down Your Mortgage One way to get rid of PMI is to simply take the purchase price of the home and multiply it by 80%. Then pay your mortgage down to that amount. So if you paid $250,000 for the home, 80% of that value is $200,000. Once you pay the loan down to $200,000, you can have the PMI removed.

Does PMI go away on conventional loans?

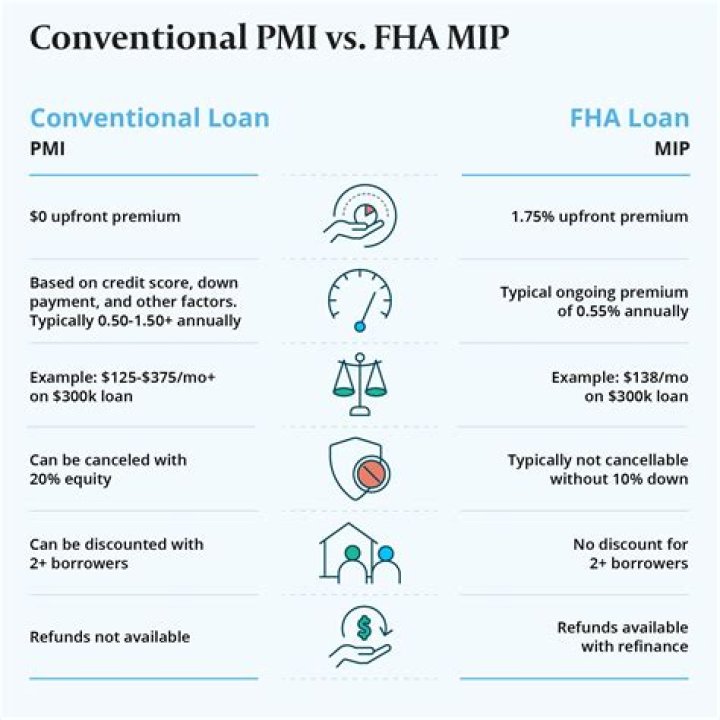

Lower Mortgage Insurance Premiums Don’t confuse this with private mortgage insurance (PMI), which is applicable only to conventional loans. Conventional loans require a 5% down payment. PMI can be removed once loan-to-value ratio (LTV) reaches 80%. Unlike PMI, MIP lasts for the life of the loan.

Do you always have to pay PMI with less than 20 down?

As a rule, most lenders require PMI for conventional mortgages with a down payment less than 20 percent.

Does PMI go towards principal?

Private mortgage insurance does nothing for you This is a premium designed to protect the lender of the home loan, not you as a homeowner. Unlike the principal of your loan, your PMI payment doesn’t go into building equity in your home.How do I get rid of PMI with equity?

To remove PMI, or private mortgage insurance, you must have at least 20% equity in the home. You may ask the lender to cancel PMI when you have paid down the mortgage balance to 80% of the home’s original appraised value. When the balance drops to 78%, the mortgage servicer is required to eliminate PMI.

Is it better to put 20 down or pay PMI?PMI is designed to protect the lender in case you default on your mortgage, meaning you don’t personally get any benefit from having to pay it. So putting more than 20% down allows you to avoid paying PMI, lowering your overall monthly mortgage costs with no downside.

Article first time published onHow do I convert my FHA to conventional?

To convert an FHA loan to a conventional home loan, you will need to refinance your current mortgage. The FHA must approve the refinance, even though you are moving to a non-FHA-insured lender. The process is remarkably similar to a traditional refinance, although there are some additional considerations.

When can I switch from FHA to conventional?

To qualify for a Streamline Refinance, you must meet these requirements: You must already have an FHA-backed mortgage. All of your mortgage payments must be up to date. You must wait 210 days or have six months of on-time payments before applying.

What is the minimum credit score for an FHA refinance?

Credit Scores According to FHA guidelines, applicants must have a minimum credit score of 580 to qualify for an FHA cash-out refinance. Most FHA insured lenders, however, set their own limits higher to include a minimum score of 600 – 620, since cash-out refinancing is more carefully approved than even a home purchase.

How do I write a letter to request PMI removal?

Dear Sirs: I am writing to request the cancellation of the Private Mortgage Insurance (PMI) policy attached to my mortgage. As you are aware, Federal law allows for the cancellation of PMI when certain LTV ratios are met through the normal amortization of a mortgage, or amortization coupled with market appreciation.

How do I request a PMI removal letter?

You have the right to request that your servicer cancel PMI when you have reached the date when the principal balance of your mortgage is scheduled to fall to 80 percent of the original value of your home. This date should have been given to you in writing on a PMI disclosure form when you received your mortgage.

Can I cancel PMI?

Once you build up at least 20 percent equity in your home, you can ask your lender to cancel this insurance. And your lender must automatically cancel PMI charges once your regular payments reduce the balance on your loan to 78 percent of your home’s original appraised value.

Can you buy out PMI?

Most lenders can offer a buy out option for conventional mortgages with private mortgage insurance. … Buying out your PMI can be as expensive as 3.29% of the loan amount with 5% down, and a 680 credit score, or 1.92% with a credit score of 760 on the same scenario.

Do credit unions waive PMI?

Zillow notes that credit unions will occasionally waive PMI for applicants on a case-by-case basis. Some financial institutions will also ask buyers with poor credit or inconsistent income to get PMI, even if they make a significant down payment.

How can I avoid PMI with 10 down?

Sometimes called a “piggyback loan,” an 80-10-10 loan lets you buy a home with two loans that cover 90% of the home price. One loan covers 80% of the home price, and the other loan covers a 10% down payment. Combined with your savings for a 10% down payment, this type of loan can help you avoid PMI.

Can you cancel PMI before 2 years?

Many loans have a “seasoning requirement” that requires you to wait at least two years before you can refinance to get rid of PMI. So if your loan is less than two years old, you can ask for a PMI-cancelling refi, but you’re not guaranteed to get approval.

Is PMI based on appraisal or purchase price?

When it comes to calculating mortgage insurance or PMI, lenders use the “Purchase price or appraised value, whichever is less” guideline. Thus, using a purchase price of $200,000 and $210,000 appraised value, the PMI rate will be based on the lower purchase price.

Is PMI based on credit score?

Credit scores and PMI rates are linked Insurers use your credit score, and other factors, to set that percentage. A borrower on the lowest end of the qualifying credit score range pays the most. “Typically, the mortgage insurance premium rate increases as a credit score decreases,” Guarino says.

Is PMI tax deductible in 2021?

Taxpayers have been able to deduct PMI in the past, and the Consolidated Appropriations Act extended the deduction into 2020 and 2021. The deduction is subject to qualified taxpayers’ AGI limits and begins phasing out at $100,000 and ends at those with an AGI of $109,000 (regardless of filing status).

Does it ever make sense to pay PMI?

Mortgage insurance can put you in a house a lot sooner. You might pay more than $100 per month for PMI. But you could start earning upwards of $20,000 per year in home equity. For many people, PMI is worth it.

How can I avoid PMI with 5% down?

The traditional way to avoid paying PMI on a mortgage is to take out a piggyback loan. In that event, if you can only put up 5 percent down for your mortgage, you take out a second “piggyback” mortgage for 15 percent of the loan balance, and combine them for your 20 percent down payment.

How can I avoid PMI without 20?

To sum up, when it comes to PMI, if you have less than 20% of the sales price or value of a home to use as a down payment, you have two basic options: Use a “stand-alone” first mortgage and pay PMI until the LTV of the mortgage reaches 78%, at which point the PMI can be eliminated. 1 Use a second mortgage.

Is Conventional better than FHA?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

Is a FHA loan worth it?

Advantages of FHA Loans Down payment: The 3.5% minimum down payment requirement on FHA loans is lower than what many (but not all) conventional loans require. If you have a credit score of about 650 or higher, the low down payment requirement is likely the main reason you’d be considering an FHA loan.

How long do you pay FHA mortgage insurance?

If you put at least 10% down on your loan, you’ll only need to pay MIP for 11 years of your loan. If you put less than 10% down, you’ll pay MIP for the entire life of your loan. You may want to wait until you have at least 10% down before you buy a home to lessen your MIP payment amount.

What is the minimum credit score for a conventional loan?

Conventional Loans A conventional loan is a mortgage that’s not insured by a government agency. Most conventional loans are backed by mortgage companies Fannie Mae and Freddie Mac. Fannie Mae says that conventional loans typically require a minimum credit score of 620.

What is the minimum down payment for a conventional loan?

The minimum down payment required for a conventional mortgage is 3%, but borrowers with lower credit scores or higher debt-to-income ratios may be required to put down more.