How are accrued expenses recorded

Understanding Accrued Expenses Accrued expenses or liabilities occur when expenses take place before the cash is paid. The expenses are recorded in a company’s balance sheet. … as current liabilities most of the time, as the payments are generally due within one year from the transaction date.

When should accruals be recorded?

You record an accrued expense when you have incurred the expense but have not yet recorded a supplier invoice (probably because the invoice has not yet been received). Accrued expenses tend to be short-term, so they are recorded within the current liabilities section of the balance sheet.

What is an accrued expense with an example?

Any expense you record now but plan to pay for at a later date creates an accrued expense account in your books. An example of an accrued expense might include: Bonuses, salaries or wages payable. … Unpaid, accrued interest payable. Utilities expenses that won’t be billed until the following month.

Where are accrued expenses recorded?

Accrued expenses are realized on the balance sheet at the end of a company’s accounting period when they are recognized by adjusting journal entries in the company’s ledger.What are accrued expenses?

Accrued expenses are those incurred for which there is no invoice or other documentation. They are classified as current liabilities, meaning they have to be paid within a current 12-month period and appear on a company’s balance sheet.

When should you record expenses?

Under the accrual basis of accounting, revenues and expenses are recorded as soon as transactions occur. This process runs counter to the cash basis of accounting, where transactions are reported only when cash actually changes hands.

How do you record accrued expenses on a balance sheet?

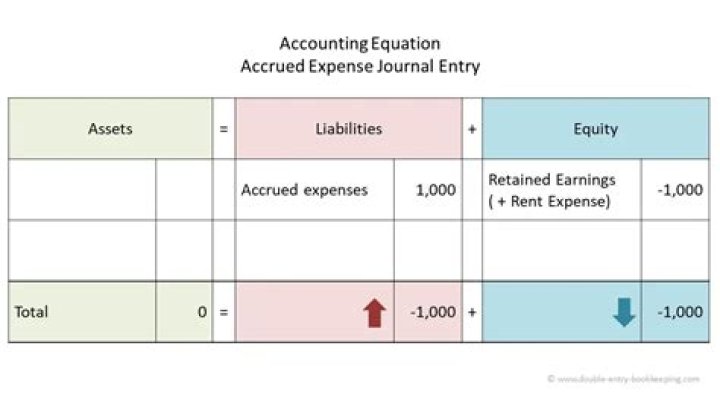

Accrued Expenses on Balance Sheet Accordingly, it should be recorded by debiting Wages and Salaries Expenses and crediting Accrued Expenses and by making an offsetting entry by debiting these expenses and crediting Cash when payment is made.

How is revenue recorded in accounting?

Revenues are recorded as Service Revenues or Sales when the service or sale has been performed, not when the cash is received. This reflects the basic accounting principle known as the revenue recognition principle.How do you record deferred expenses?

Accounting for Deferred Expenses Like deferred revenues, deferred expenses are not reported on the income statement. Instead, they are recorded as an asset on the balance sheet until the expenses are incurred. As the expenses are incurred the asset is decreased and the expense is recorded on the income statement.

What does accrued mean in accounting?An accrual is an accounting adjustment used to track and record revenues that have been earned but not received, or expenses that have been incurred but not paid. … 1 Accruals can include accounts payable, accounts receivable, goodwill, future tax liability, and future interest expense.

Article first time published onHow do you record expenses in accounting?

- Debit to expense, credit to cash. Reflects a cash payment.

- Debit to expense, credit to accounts payable. Reflects a purchase made on credit.

- Debit to expense, credit to asset account. …

- Debit to expense, credit to other liabilities account.

What do you mean by accrue?

Definition of accrue intransitive verb. 1 : to come into existence as a legally enforceable claim. 2a : to come about as a natural growth, increase, or advantage the wisdom that accrues with age. b : to come as a direct result of some state or action rewards due to the feminine will accrue to me— Germaine Greer.

What are accruals give 2 examples?

- Sales on Credit.

- Purchase on Credit.

- Income Tax Expenses.

- Rent Paid in Advance.

- Interest Received on FD.

- Insurance Expenses. You can calculate it as a fixed percentage of the sum insured & it is paid at a daily pre-specified period.

- Electricity Expenses.

- Post-sales Discount.

Are salaries accrued expenses?

Salary and wages payable, interest and other expenses like loan interest or taxes can all be considered accrued expenses.

Is rent an accrued expense?

Accrued rent expense is the amount of rent cost that has been incurred by a renter during a reporting period, but not yet paid to the landlord. In practice, this amount is small to nonexistent, since landlords typically insist on rent being paid in advance.

How do you record accrued revenue?

Accrued revenue is recorded in the financial statements by way of an adjusting journal entry. The accountant debits an asset account for accrued revenue which is reversed when the exact amount of revenue is actually collected, crediting accrued revenue.

How do you record accrued utilities?

Utilities expense journal entry without current period invoice. The company can make the utilities expense journal entry by debiting the utilities expense account and crediting the accounts payable at the period-end adjusting entry.

Why are accrued expenses important?

Accruals adjust the revenues earned and expenses incurred by a company when no cash has been exchanged. Accruals are important because they help a company to keep track of its financial position more accurately and systematically.

Where are expenses recorded on a balance sheet?

In short, expenses appear directly in the income statement and indirectly in the balance sheet. It is useful to always read both the income statement and the balance sheet of a company, so that the full effect of an expense can be seen.

Do you include GST in accrued expenses?

(iii) Unlike accounts payable, accrued expenses are recognised exclusive of the amount of Goods and Services Tax (GST) as GST relating to the transaction is recognised at the earlier of arrival of a tax invoice or payment of cash.

What is the difference between deferred expense and accrued expense?

An accrued expense is a liability that represents an expense that has been recognized but not yet paid. A deferred expense is an asset that represents a prepayment of future expenses that have not yet been incurred.

What is the difference between accrued and deferred expense?

Deferred revenue, also known as unearned revenue, refers to advance payments a company receives for products or services that are to be delivered or performed in the future. Accrued expenses refer to expenses that are recognized on the books before they have actually been paid.

What are the 3 types of expenses?

There are three major types of expenses we all pay: fixed, variable, and periodic.

What is an example of deferred expense?

Common examples of deferred expenditures include: Advertising fees. Advance payment of insurance coverage. An intangible asset cost that is deferred due to amortisation. Tangible asset depreciation costs.

What is the difference between prepaid and advance?

As nouns the difference between prepayment and advance is that prepayment is a payment in advance while advance is a forward move; improvement or progression.

What does deferred mean in accounting?

In accounting, a deferral refers to the delay in recognition of an accounting transaction. This can arise with either a revenue or expense transaction. … In the case of the deferral of an expense transaction, you would debit an asset account instead of an expense account.

How do you recognize revenue and expenses under accrual accounting?

The accrual basis of accounting recognizes revenues when earned (a product is sold or a service has been performed), regardless of when cash is received. Expenses are recognized as incurred, whether or not cash has been paid out. For instance, assume a company performs services for a customer on account.

Is revenue recorded as debit or credit?

Account TypeNormal BalanceRevenueCREDITExpenseDEBITException:DividendsDEBIT

How do you record expenses in a general ledger?

Include the general ledger account number and title (specific to your company), debit office supplies expense for $100 and credit cash for $100. A brief description may be “purchased office supplies.” Enter the journal entry into the general ledger. If you use a paper ledger, hand write the entry into the ledger.

How does an accrual work?

Using accruals, companies record expenses when incurred with or without any cash payments for the expenses. To record an expense in the period in which it is incurred, companies debit the expense account and credit the accounts payable, an account used to track the amount of cash owed by the company to suppliers.

What accounts are under expenses?

Some common expense accounts are: Cost of sales, utilities expense, discount allowed, cleaning expense, depreciation expense, delivery expense, income tax expense, insurance expense, interest expense, advertising expense, promotion expense, repairs expense, maintenance expense, rent expense, salaries and wages expense, …