How can I avoid PMI with 10% down

Sometimes called a “piggyback loan,” an 80-10-10 loan lets you buy a home with two loans that cover 90% of the home price. One loan covers 80% of the home price, and the other loan covers a 10% down payment. Combined with your savings for a 10% down payment, this type of loan can help you avoid PMI.

How much money do you have to put down on a conventional loan?

The minimum down payment required for a conventional mortgage is 3%, but borrowers with lower credit scores or higher debt-to-income ratios may be required to put down more. You’ll also likely need a larger down payment for a jumbo loan or a loan for a second home or investment property.

Do conventional loans require 5% down?

It is a common misconception that in order to obtain a conventional loan, you must pay a 20% down payment, but that is not the case. In fact, you can qualify for a conventional loan by putting down as low as a 5% down payment.

Do all conventional loans require 20 down?

Typically, conventional loans require PMI when you put down less than 20 percent. … Most lenders offer conventional loans with PMI for down payments ranging from 5 percent to 15 percent. Some lenders may offer conventional loans with 3 percent down payments. A Federal Housing Administration (FHA) loan.Do you need PMI with 10 down?

With an “80-10-10” piggyback mortgage, for example, 80% of the purchase price is covered by the first mortgage, 10% is covered by the second loan, and the final 10% is covered by your down payment. This lowers the loan-to-value (LTV) of the first mortgage to under 80%, eliminating the need for PMI.

Can you put 3 down on a conventional loan?

Can I get a mortgage with 3% down? Yes! The conventional 97 program allows 3% down and is offered by many lenders. Fannie Mae’s HomeReady loan and Freddie Mac’s Home Possible loan also allow 3% down with extra flexibility for income and credit qualification.

Do conventional loans require PMI?

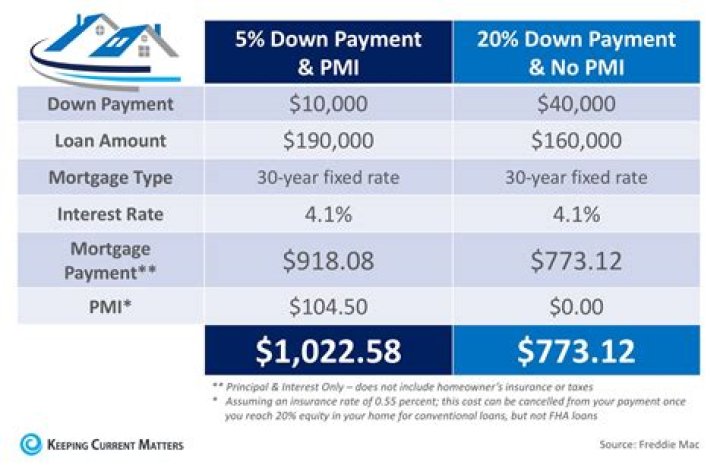

If you put down less than 20% on a conventional loan, you’ll be required to pay for private mortgage insurance (PMI). PMI protects your lender in case you default on your loan. The cost for PMI varies based on your loan type, your credit score and the size of your down payment.

Is Conventional better than FHA?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.Is it better to put 20 down or pay PMI?

PMI is designed to protect the lender in case you default on your mortgage, meaning you don’t personally get any benefit from having to pay it. So putting more than 20% down allows you to avoid paying PMI, lowering your overall monthly mortgage costs with no downside.

Can you buy a fixer upper with a conventional loan?You can certainly buy a fixer-upper with a conventional loan, and many people do, but you’ll still need a plan on how you’ll finance the renovations. … This loan type allows you to combine both the purchase and renovation of the property into one long-term, fixed-rate mortgage.

Article first time published onHow can I avoid PMI with 5% down?

The traditional way to avoid paying PMI on a mortgage is to take out a piggyback loan. In that event, if you can only put up 5 percent down for your mortgage, you take out a second “piggyback” mortgage for 15 percent of the loan balance, and combine them for your 20 percent down payment.

How can you avoid PMI without 20 down?

To sum up, when it comes to PMI, if you have less than 20% of the sales price or value of a home to use as a down payment, you have two basic options: Use a “stand-alone” first mortgage and pay PMI until the LTV of the mortgage reaches 78%, at which point the PMI can be eliminated. 1 Use a second mortgage.

What happens if you don't put 20 down on a house?

What happens if you can’t put down 20%? If your down payment is less than 20% and you have a conventional loan, your lender will require private mortgage insurance (PMI), an added insurance policy that protects the lender if you can’t pay your mortgage.

How much should I put down on a 200k house?

Conventional mortgages, like the traditional 30-year fixed rate mortgage, usually require at least a 5% down payment. If you’re buying a home for $200,000, in this case, you’ll need $10,000 to secure a home loan. FHA Mortgage. For a government-backed mortgage like an FHA mortgage, the minimum down payment is 3.5%.

How much should you put down on a 300k house?

Fannie Mae and Freddie Mac (the agencies that set rules for conforming mortgages) require a down payment of only 3% of the purchase price. That’s $9,000 on a $300,000 home – the lowest possible unless you’re eligible for a zero–down–payment VA or USDA loan.

How much house can I afford if I make 3000 a month?

For example, if you make $3,000 a month ($36,000 a year), you can afford a mortgage with a monthly payment no higher than $1,080 ($3,000 x 0.36). Your total household expense should not exceed $1,290 a month ($3,000 x 0.43).

Why would a seller want a conventional loan?

Length of Time to Close. By and large, conventional loans simply tend to close faster. Less paperwork and fewer stipulations allow these mortgages to be processed more quickly, and many sellers find this to be an attractive bonus.

What are the pros and cons of a conventional loan?

- Credit Considerations. Riskier than mortgages backed by the US government, conventional loans typically hold borrowers to a higher standard. …

- Money Down & Mortgage Insurance. …

- More Options. …

- Time & Cost to Close. …

- A Seller’s Market.

Is it hard to get a conventional home loan?

Even though a conventional loan is the most common mortgage, it is surprisingly difficult to get. Borrowers need to have a minimum credit score of about 640 in order to qualify—the highest minimum score of all mortgage products—and have a debt-to-income ratio of 43% or less.

Is 203k a conventional loan?

FHA 203(k) Loan Offered by the U.S. Department of Housing and Urban Development (HUD), this loan is backed and insured by the FHA. While only approved lenders, such as Contour Mortgage, can offer these, they also have slightly more lenient terms than conventional mortgages.

Can you add renovation costs to a conventional mortgage?

Conventional options The loan also has a refinance option for homeowners who want to update their current property.” Borrowers can finance renovations that cost up to 75 percent of a home’s value after renovations, as long as they qualify for the total loan amount.

What credit score do you need to qualify for a conventional home loan?

According to mortgage company Fannie Mae, a conventional loan usually requires a credit score of at least 620.

How can I lower my PMI on my conventional loan?

- Improve your credit score. …

- Make a larger down payment. …

- Choose a fixed loan over an ARM.

- Choose a loan with a term of 20 years or fewer.

Is PMI based on credit score?

Credit scores and PMI rates are linked Insurers use your credit score, and other factors, to set that percentage. A borrower on the lowest end of the qualifying credit score range pays the most. “Typically, the mortgage insurance premium rate increases as a credit score decreases,” Guarino says.

Is PMI tax deductible?

A PMI tax deduction is only possible if you itemize your federal tax deductions. … The standard deduction for 2020 was $12,400 for single taxpayers or $24,800 for married couples filing jointly, and it’s increasing to $12,550 for single filers and $25,100 for couples for the 2021 tax year.

Is PMI tax deductible in 2021?

Taxpayers have been able to deduct PMI in the past, and the Consolidated Appropriations Act extended the deduction into 2020 and 2021. The deduction is subject to qualified taxpayers’ AGI limits and begins phasing out at $100,000 and ends at those with an AGI of $109,000 (regardless of filing status).

Does PMI go towards principal?

Private mortgage insurance does nothing for you This is a premium designed to protect the lender of the home loan, not you as a homeowner. Unlike the principal of your loan, your PMI payment doesn’t go into building equity in your home.

Can you avoid PMI with a high credit score?

The tradeoff here is that no–PMI loans usually have higher rates. And, they often require a higher credit score to qualify. Keep in mind that lenders can change proprietary mortgage programs at any time.

How much do I need to make to buy a 400k house?

What income is required for a 400k mortgage? To afford a $400,000 house, borrowers need $55,600 in cash to put 10 percent down. With a 30-year mortgage, your monthly income should be at least $8200 and your monthly payments on existing debt should not exceed $981.

What is the average down payment on a house in 2021?

In 2021, the National Association of Realtors found the average down payment on a house or condo was just 12%. For home buyers aged 30 and under, that number drops to 6%. And many people put down even less money – or no money at all. Check a few loan programs to see how much you need to put down on your new home loan.

What are the disadvantages of a large down payment?

- Longer time to enter the market. The months or years spent saving for a large down payment can delay your readiness to buy a house. …

- Less short-term flexibility. …

- Interference with investments or retirement saving. …

- Benefits take a while to add up.