How do you calculate deferred tax assets

If the tax rate for the company is 30%, the difference of $18 ($60 x 30%) between the taxes payable in the income statement and the actual taxes paid to the tax authorities is a deferred tax asset.

What is the formula for calculating deferred tax?

It is calculated as the company’s anticipated tax rate times the difference between its taxable income and accounting earnings before taxes. Deferred tax liability is the amount of taxes a company has “underpaid” which will be made up in the future.

What is included in deferred tax asset?

Deferred tax assets are items that may be used for tax relief purposes in the future. Usually, it means that your business has overpaid tax or has paid tax in advance, so it can expect to recoup that money later. This sometimes happens because of changes in tax rules that occur in the middle of the tax year.

How do you calculate deferred tax assets and liabilities?

Temporary timing differences create deferred tax assets and liabilities. Deferred tax assets indicate that you’ve accumulated future deductions—in other words, a positive cash flow—while deferred tax liabilities indicate a future tax liability.Why is nol a deferred tax asset?

(NOL) Net Operating Loss Carryforward Explained: Losses Become Assets. In contrast to deferred tax liabilities, a net operating loss (NOL) carryforward is a number that can be used to offset future Net Income, which creates a deferred tax asset on a balance sheet that represents a future tax deduction.

Are deferred tax assets Current assets?

Deferred taxes are a non-current asset for accounting purposes. A current asset is any asset that will provide an economic benefit for or within one year. Deferred taxes are items on the balance sheet that arise from overpayment or advance payment of taxes, resulting in a refund later.

What is deferred tax example?

During the periods of rising costs and when the company’s inventory takes a long time to sell, the temporary differences between tax and financial books arise, resulting in deferred tax liability. Consider an oil company with a 30% tax rate that produced 1,000 barrels of oil at a cost of $10 per barrel in year one.

What gives deferred tax assets rise?

A deferred tax asset is an item on the balance sheet that results from the overpayment or the advance payment of taxes. … A deferred tax asset can arise when there are differences in tax rules and accounting rules or when there is a carryover of tax losses.What is the journal entry for deferred tax asset?

The accounting entry to record additions to deferred tax assets debits (increases) the Deferred Tax Asset account and credits (reduces) Income Tax Expense. The income statement may actually show a “net tax benefit” (negative tax expense) in the year the firm files a tax return with a NOL.

How are deferred tax assets realized?Deferred tax assets are realizable if the future deductible amounts would, under the existing provisions of the tax law, result in future tax losses that can be carried back to recover taxes paid for the current year or prior years within the carryback period. Future Reversals of Existing Taxable Temporary Differences.

Article first time published onWhere is deferred tax asset balance sheet?

It is shown under the head of Non- Current Assets in the balance sheet. It is shown under the head of Non- Current Liability in the balance sheet. It is important to mention that both the deferred tax asset and deferred tax liability are created for the temporary differences only.

Is an NOL a deferred tax asset?

The full loss from the first year can be carried forward on the balance sheet to the second year as a deferred tax asset.

Is deferred tax asset an estimate?

The Group believes that the accounting estimate related to the deferred tax assets is a critical accounting estimate because the underlying assumptions can change from period to period. …

How does tax deferred savings work?

A tax-deferred savings plan is an investment account that allows a taxpayer to postpone paying taxes on the money invested until it is withdrawn, generally after retirement. The best-known such plans are individual retirement accounts (IRAs) and 401(k)s.

Is a 401k a tax deferred asset?

A 401(k) is a tax-deferred account. That means you do not pay income taxes when you contribute money. Instead, your employer withholds your contribution from your paycheck before the money can be subjected to income tax. … Instead, you defer paying those taxes until you withdraw the money.

Is a deferred tax asset a tangible asset?

Deferred tax assets are assets for which the holder does not need to pay taxes until a certain point. In most cases, deferred tax assets are considered tangible.

Are prepaid taxes a deferred tax asset?

In accounting, Prepaid Income Tax is defined as an asset listed on the balance sheet that represents taxes that have been already paid despite not yet having been incurred. It is also called a deferred income tax asset.

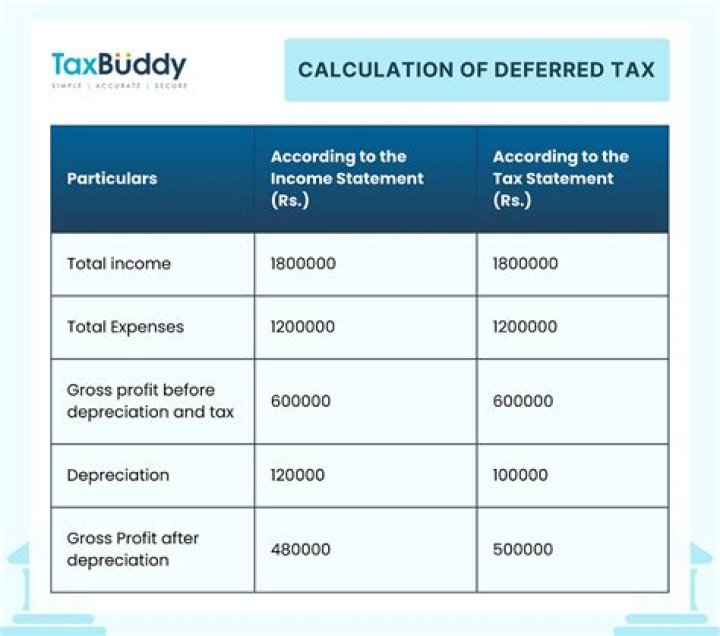

What is deferred tax and why to calculate Have you calculated?

The term deferred tax, in essence, refers to the tax which shall either be paid or has already been settled due to transient inconsistency between an organisation’s income statement and tax statement. As per this definition, there are two types of deferred tax-deferred tax asset and deferred tax liability.

How is deferred tax calculated on Wdv basis?

COMPUTATION OF DEFERRED TAXAmount (Rs.)WDV of Assets as per Income Tax Act v/s Companies ActWDV as per IT act25,000,000WDV as per Companies Act33,000,000