How does a buy down mortgage work

A mortgage rate buydown is when a borrower pays an additional charge in exchange for a lower interest rate on their mortgage. Just like lenders can help cover the borrower’s closing costs by charging a slightly higher interest rate, the door swings both ways. Borrowers can essentially buy a lower interest rate upfront.

What is a mortgage buy down?

A buydown is a way for a borrower to obtain a lower interest rate by paying discount points at closing. Discount points, also referred to as mortgage points or prepaid interest points, are a one-time fee paid upfront.

How does a buydown loan work?

A buydown is a mortgage-financing technique that allows a homebuyer to obtain a lower interest rate for at least the first few years of the loan, or possibly its entire life, in return for an extra up-front payment.

What is the qualifying rate on a 2 1 buy down?

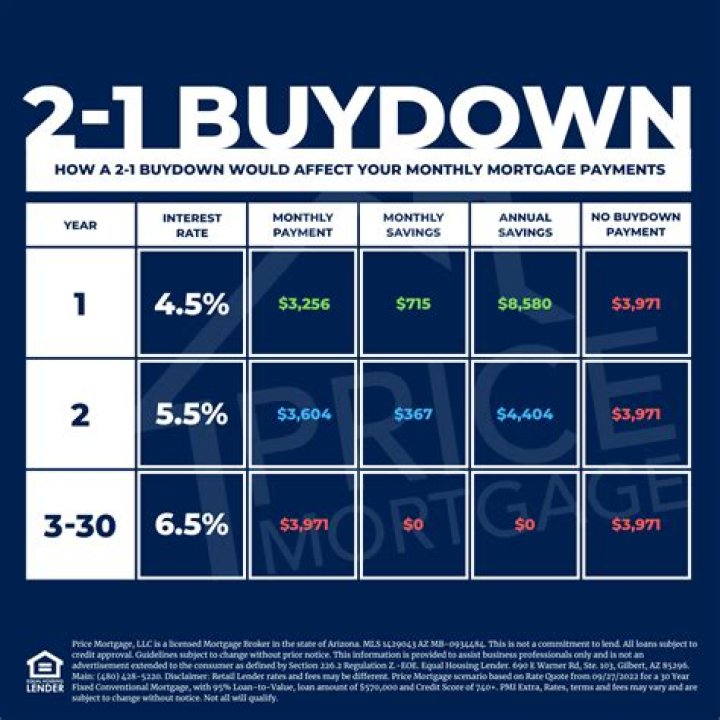

A 2/1 buy down (pronounced “two one buy down”) means that your mortgage interest rate starts two percent (2%) below the actual rate. That “teaser rate” is only for the first year of the loan.How are temporary buydown typically paid for?

The monthly payments reflect the rate at the time, so the payments are lower during the first two years than they are for the remaining years. The money put towards the buydown is put into an escrow account and is paid to the lender to make up the difference.

What is a two step mortgage?

A two-step mortgage is a mortgage that has both an introductory rate for a lender, and then a higher rate beyond the initial borrowing period.

Is 3.125 a good mortgage interest rate?

Throughout the first half of 2021, the best mortgage rates have been in the high–2% range. And a ‘good’ mortgage rate has been around 3% to 3.25%.

What does PITI stand for?

PITI is an acronym that stands for principal, interest, taxes and insurance. Many mortgage lenders estimate PITI for you before they decide whether you qualify for a mortgage.Does PITI include mortgage insurance?

Principal, interest, taxes, insurance (PITI) are the sum components of a mortgage payment. Specifically, they consist of the principal amount, loan interest, property tax, and the homeowners insurance and private mortgage insurance premiums.

What is a 7 23 mortgage?General Overview. 7/23 Balloon mortgage – the rate is fixed for a period of 7 years and then converts to a new fixed rate for the remaining 23 years. The new rate is typically based on the Fannie Mae 60 day net yield index and is added to a pre-determined margin, usually 0.500.

Article first time published onWhat is a permanent interest rate buydown?

A permanent buydown mortgage has a lower interest rate for the entire term of the loan. So, if a borrower gets a 30-year fixed rate mortgage with a permanent buydown, the interest rate will be lower for all 30 years. … it takes 3-6 years to break even from buying down a mortgage.

How much does 1 point lower your interest rate?

Each point typically lowers the rate by 0.25 percent, so one point would lower a mortgage rate of 4 percent to 3.75 percent for the life of the loan.

What is a 1 1 buydown?

1-1-1 Buydown: A payment rate 1% lower than the note rate for the first three years on a new loan.

What is a permanent buydown?

A buydown is a type of financing where the buyer or seller pays extra points (also called discount points) to reduce the interest rate on a loan. … A permanent buydown lets you pay extra points to get a low interest rate over the life of your loan.

Which of the following is a description of a permanent buy down?

Which of the following is a description of a permanent buy-down? A borrower pays discount points to lower the note rate from 4.875 to 4.50. A permanent buy-down is a tool some borrowers use to adjust the price of their loan. It can also be referred to as prepaying interest.

Can I lose my good faith deposit?

In most real estate markets, the average good faith deposit is between 1% and 3% of the property’s purchase price. … While losing your good faith deposit is unlikely, offer an amount that the seller will appreciate without exposing yourself to financial risk.

Is 3% interest on a mortgage good?

Anything at or below 3% is an excellent mortgage rate. And the lower, your mortgage rate, the more money you can save over the life of the loan. … As you can see, just one percentage point could save you nearly $50,000 in interest payments for your mortgage.

Are interest rates going up in 2021?

Today, a number of major mortgage rates climbed higher. We also saw an increase in the average rate of 5/1 adjustable-rate mortgages. …

What is a good tip mortgage?

When you shop for a mortgage you want the lowest rate, say 3.75 percent rather than 4 percent. … According to the Consumer Financial Protection Bureau, the TIP tells you how much interest you will pay over the life of your mortgage loan, compared to the amount you borrowed.

What is Readvanceable mortgage?

A readvanceable mortgage is a type of mortgage that allows the borrower to add a line of credit to the loan, permitting the borrower to re-borrow any part of the principal paid down. It is essentially a primary mortgage bundled with a home equity line of credit (HELOC).

What is a step mortgage?

What is STEP? The Scotia Total Equity Plan (STEP) is a flexible borrowing plan tied to the equity in your home. STEP lets you choose from different kinds of Scotiabank credit products (like mortgages, a line of credit, credit cards and more) based on your needs, all with one easy application. 1.

What is hybrid ARM?

A 30 year Mortgage Loan, comprised of an initial term where interest accrues at a fixed rate, after which it automatically converts to accrue interest at an adjustable rate for the remaining term.

Do you pay taxes upfront when buying a house?

Pre-Paid Property Taxes Your upfront pre-paid tax payments when you buy a home are normally due on the day you close on your home.

What does PMI stand for?

Private mortgage insurance (PMI) is a type of insurance that may be required by your mortgage lender if your down payment is less than 20 percent of your home’s purchase price. PMI protects the lender against losses if you default on your mortgage.

What are the upfront costs of buying a home?

Upfront costs are the costs you pay out of pocket once your offer on a home has been accepted. Upfront costs include earnest money, the inspection fee, and the appraisal fee. Appraisal fee: typically $300–$500, paid after inspection and on or before closing.

How much PITI can I afford?

In total, your PITI should be less than 28 percent of your gross monthly income, according to Sethi. For example, if you make $3,500 a month, your monthly mortgage should be no higher than $980, which would be 28 percent of your gross monthly income.

Does your home become collateral when you take out a mortgage?

When you take out a mortgage, your home becomes the collateral. If you take out a car loan, then the car is the collateral for the loan. … Retirement accounts are not usually accepted as collateral. You also may use future paychecks as collateral for very short-term loans, and not just from payday lenders.

Is an escrow account good or bad?

Escrows are not all bad. There are good reasons to maintain an escrow: … The lender benefits by having an escrow in place for taxes and insurance because it protects them against the risk of the collateral for their loan (your home) being auctioned off by the county if those expenses are not paid.

How much is a balloon payment?

The term “balloon” indicates that the final payment is significantly large. Balloon payments tend to be at least twice the amount of the loan’s previous payments.

How is the balloon payment calculated?

Your balloon payment is calculated by the lender at the start of your agreement, based on the Guaranteed Future Value (GFV) of the vehicle. This is the resale value the lender predicts your vehicle to be worth at the end of your contract.

What is bubble loan?

In this type of loan with no balloon payment, his/her entire loan will be amortised in small monthly payments till the time his/her entire loan is paid. If there is balloon payment involved then, usually, the entire principal payment is paid in lump sum towards the end of the term.