How many banks failed in 2020

There were 4 bank failures in 2020. See detailed descriptions below. Please select the buttons below for other years’ information.

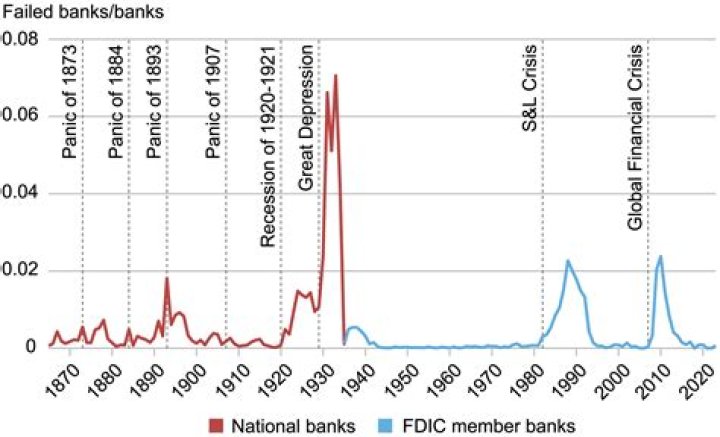

How many banks fail every year?

YearBank failure cost to Deposit Insurance Fund (DIF)Total number of bank failures: 5112018$0 (estimated)02017$1.31 billion (estimated)82016$9.6 million (estimated)52015$894 million (estimated)8

Why do banks fail in modern times?

Poor corporate governance has been cited as one of the major causes of the collapse of the seven banks by BoG, and other financial analysts. Board level and senior management were either inactive or engaged in activities that inured to their personal interests rather than to the growth of the banks.

Why do most banks fail?

The most common cause of bank failure occurs when the value of the bank’s assets falls to below the market value of the bank’s liabilities, which are the bank’s obligations to creditors and depositors. This might happen because the bank loses too much on its investments.Are banks in trouble 2021?

As the US economy continues to recover, banks have reported spectacular profits in 2021. … But consumer banking revenues declined 3% in Q2 2021 from the prior quarter and was down 7% from the same period a year ago.

Are banks shutting down in us?

According to National Community Reinvestment Coalition, the number of bank branches in the U.S. declined by 5.1% between 2017 and 2020 to 81,586. Since the financial crisis of 2008, the annual pace of closures has accelerated – as such, more than 4,400 branches shuttered during 2017-2020 alone.

Are banks going to fail in 2021?

U.S. banks are bracing for worse credit quality in 2021 as COVID-19 remains active, triggering new lockdown orders and weighing on consumer confidence. Bank failures spiked after the Great Recession but have been rare in recent years. …

Which banks are most likely to fail?

- JPMorgan Chase.

- Citigroup.

- Bank of America.

- Morgan Stanley.

- Goldman Sachs.

- Wells Fargo.

- Bank of New York Mellon.

- State Street.

Did banks fail 2008?

The Financial crisis of 2007–2008 led to many bank failures in the United States. The Federal Deposit Insurance Corporation (FDIC) closed 465 failed banks from 2008 to 2012. In contrast, in the five years prior to 2008, only 10 banks failed.

Will you lose your money if your bank fails?If your bank is insured by the Federal Deposit Insurance Corporation (FDIC) or your credit union is insured by the National Credit Union Administration (NCUA), your money is protected up to legal limits in case that institution fails. This means you won’t lose your money if your bank goes out of business.

Article first time published onCan banks seize your money?

Banks may freeze bank accounts if they suspect illegal activity such as money laundering, terrorist financing, or writing bad checks. Creditors can seek judgment against you which can lead a bank to freeze your account. The government can request an account freeze for any unpaid taxes or student loans.

What happens to your money if a bank collapses?

When a bank fails, the FDIC reimburses account holders with cash from the deposit insurance fund. The FDIC insures accounts up to $250,000, per account holder, per institution. Individual Retirement Accounts are insured separately up to the same per bank, per institution limit.

Is my money safe in the bank 2021?

In times of economic unease, you may find yourself wondering whether your money is safe in your bank account. … The good news is that your money is absolutely safe in a bank — there’s no need to withdraw it for security reasons.

Can the FDIC fail?

CoveredNot CoveredChecking accountsStocks and bondsSavings accountsMutual funds

What is the largest bank failure in US history?

Washington Mutual was a conservative savings and loan bank. In 2008, it became the largest failed bank in U.S. history.

What banks no longer exist?

- A. G. Becker & Co.

- Advanta.

- American Fletcher National Bank.

- American Savings and Loan.

- American Southern Bank.

- American State Bank.

- American Sterling Bank.

- Amresco.

How many saving accounts were wiped out?

The Great Depression was an economic crisis of a magnitude never before seen in the United States. During this time, stock prices plummeted, 9,000 banks went out of business, 9 million savings accounts were wiped out, 86,000 businesses failed and wages decreased by an average of 60%.

Why are banks closing accounts?

A bank generally can close your account at any time and for any reason—and sometimes without notifying you in advance. Reasons a bank may shut down your account include using your account very little or not at all, or bouncing too many checks.

Why are all the banks closing?

Indeed, the driving force behind the upswing in bank branch closings is the increased use of online and mobile banking. Customers can complete most, if not all, of their financial transactions digitally, which creates a waning demand for branch offices.

Why are Barclays closing so many branches?

The bank told the BBC it had decided to close these particular branches as customers were ‘increasingly using alternatives to branches to do their banking‘.

Can a bank be too big to fail?

Reasons why ‘too big to fail’ is a useful policy: The failure of the bank can lead to systematic risk, which is threatening the whole banking system. The failure of large institutions can immediately cause failures of other industries in the whole financial system.

What year did the banks collapse?

November 1930–August 1931. The U.S. appeared to be poised for economic recovery following the stock market crash of 1929, until a series of bank panics in the fall of 1930 turned the recovery into the beginning of the Great Depression.

What happened to Bear Stearns?

Bear Stearns was a New York City-based global investment bank and financial company that was founded in 1923. It collapsed during the 2008 financial crisis. … The company was ultimately sold to JPMorgan Chase for $10 a share, well below its value before the crisis.

How do you shrink too big to fail banks?

Solutions. The proposed solutions to the “too big to fail” issue are controversial. Some options include breaking up the banks, introducing regulations to reduce risk, adding higher bank taxes for larger institutions, and increasing monitoring through oversight committees.

Is Bank of America financially stable?

Fitch Affirms Bank of America at ‘A+’/’F1’; Outlook Stable Despite Coronavirus Impact. … The Rating Outlook remains Stable even though Fitch expects significant operating environment headwinds due to the disruption to economic activity and financial markets from the coronavirus pandemic.

Has FDIC ever been used?

FDICAgency overviewFormedJune 16, 1933JurisdictionFederal government of the United StatesEmployees5,538 (2020)

How much money should you keep in the bank?

Most financial experts end up suggesting you need a cash stash equal to six months of expenses: If you need $5,000 to survive every month, save $30,000. Personal finance guru Suze Orman advises an eight-month emergency fund because that’s about how long it takes the average person to find a job.

What happens if you have more than 250 000 in bank?

Bottom line. Any individual or entity that has more than $250,000 in deposits at an FDIC-insured bank should see to it that all monies are federally insured. And it’s not only diligent savers and high-net-worth individuals who might need extra FDIC coverage.

Should I take all my money out of the bank?

The good news is that your money is absolutely safe in a bank — there’s no need to withdraw it for security reasons. Here’s more about bank runs and why they shouldn’t be a concern, thanks to the system that protects your deposits.

Is offshore banking illegal?

There’s nothing illegal about establishing an offshore account unless you do it with the intent of tax evasion. The Foreign Account Tax Compliance Act (FATCA) requires banks around the world to report balances and any activity of American citizens to the IRS or face fines.

How can creditors find my bank account?

A creditor can merely review your past checks or bank drafts to obtain the name of your bank and serve the garnishment order. If a creditor knows where you live, it may also call the banks in your area seeking information about you.