Is a conventional loan better

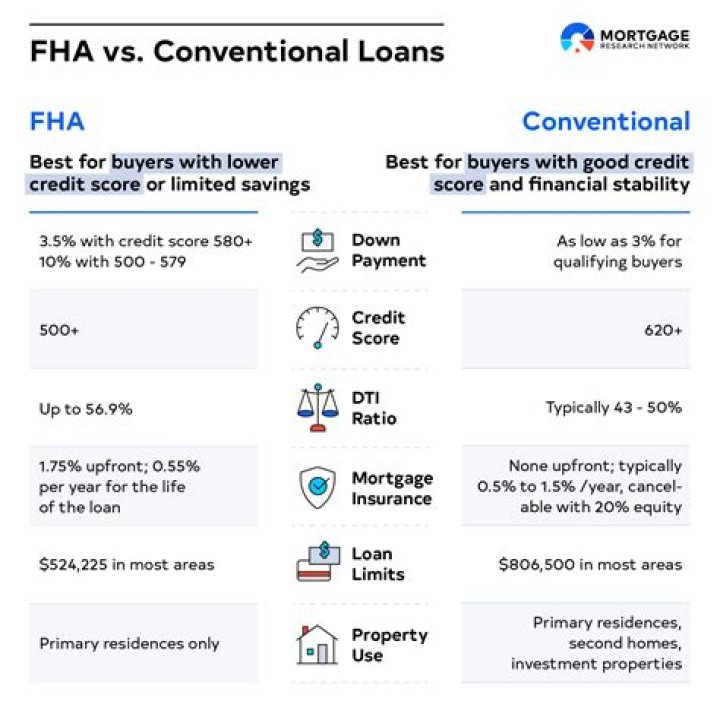

A conventional loan is better in the sense that it’s less expensive if you have excellent credit and a 20% down payment. You may qualify for lenders’ best interest rates and you won’t have to pay for private mortgage insurance. An FHA loan is better if your credit score isn’t great.

What is the downside of a conventional loan?

A disadvantage to conventional lending is generally lower debt-to-income ratios are required. Low income and high debt scenarios pose additional risk to private lenders, therefore debt ratio requirements are more stringent with conventional loans.

Is it good to get a conventional loan?

A conventional loan is a great option if you have a solid credit score and little debt. You can avoid PMI by paying 20% of the loan upfront, which will lower your mortgage payments. If you’re unable to make a large payment upfront, conventional loans are available with a down payment as low as 3%.

Is it better to go FHA or conventional?

FHA loans are great for low–to–average credit. They allow credit scores starting at just 580 with a 3.5% down payment. But FHA mortgage insurance is always required. Conventional loans are often better if you have great credit, or plan to stay in the house a long time.Why would a seller want a conventional loan?

Length of Time to Close. By and large, conventional loans simply tend to close faster. Less paperwork and fewer stipulations allow these mortgages to be processed more quickly, and many sellers find this to be an attractive bonus.

What's the minimum down payment for a conventional loan?

The minimum down payment required for a conventional mortgage is 3%, but borrowers with lower credit scores or higher debt-to-income ratios may be required to put down more. You’ll also likely need a larger down payment for a jumbo loan or a loan for a second home or investment property.

Can I put 3 down on a conventional loan?

Can I get a mortgage with 3% down? Yes! The conventional 97 program allows 3% down and is offered by many lenders. Fannie Mae’s HomeReady loan and Freddie Mac’s Home Possible loan also allow 3% down with extra flexibility for income and credit qualification.

Do conventional loans require PMI?

If you put down less than 20% on a conventional loan, you’ll be required to pay for private mortgage insurance (PMI). PMI protects your lender in case you default on your loan. The cost for PMI varies based on your loan type, your credit score and the size of your down payment.What are the pros and cons of a conventional loan?

- Credit Considerations. Riskier than mortgages backed by the US government, conventional loans typically hold borrowers to a higher standard. …

- Money Down & Mortgage Insurance. …

- More Options. …

- Time & Cost to Close. …

- A Seller’s Market.

Closing costs for FHA loans are about the same as they are for conventional loans, with a couple exceptions. The FHA home appraisal is a little more complicated than the standard appraisal, and it often costs about $50 more. FHA requires an upfront mortgage insurance premium (MIP) of 1.75 percent of your loan amount.

Article first time published onCan you finance closing costs on a conventional loan?

When you buy a home, you typically don’t have an option to finance the closing costs. Closing costs must be paid by the buyer or the seller (as a seller concession).

Can you put 5 down on a conventional loan?

Conventional loans require buyers to make a minimum 5 percent downpayment on a home. Because this is a conventional loan, and because the downpayment is less than twenty percent, private mortgage insurance (PMI) will be required.

What credit score is needed for conventional home loan?

According to mortgage company Fannie Mae, a conventional loan usually requires a credit score of at least 620. But you may qualify for a government-sponsored loan with a lower score. Read on to learn more about credit scores and how they impact the homebuying process.

Do conventional loans appraise higher?

Once you apply for an FHA loan, one of the loan requirements is that the home appraisal is done at a higher standard as compared to the conventional appraisal. The FHA loan has a minimum down payment requirement but conventional loan has a higher down payment requirement despite its lower standards.

Why are some homes conventional Only?

Some sellers will have their home listed on the market allowing only a Cash or Conventional loan buyer to make offers on it. … The usual reason for this is because the appraisal done on an FHA or VA loan is a little more stringent with it’s requirements for the property to meet the government FHA or VA standards.

Why do buyers prefer conventional over FHA?

Conventional Loans. FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

Who pays for closing costs?

Closing costs are paid according to the terms of the purchase contract made between the buyer and seller. Usually the buyer pays for most of the closing costs, but there are instances when the seller may have to pay some fees at closing too.

Should I put 20 down or pay PMI?

PMI is designed to protect the lender in case you default on your mortgage, meaning you don’t personally get any benefit from having to pay it. So putting more than 20% down allows you to avoid paying PMI, lowering your overall monthly mortgage costs with no downside.

How can I avoid PMI with 5% down?

The traditional way to avoid paying PMI on a mortgage is to take out a piggyback loan. In that event, if you can only put up 5 percent down for your mortgage, you take out a second “piggyback” mortgage for 15 percent of the loan balance, and combine them for your 20 percent down payment.

Do sellers prefer conventional loans?

“If there are multiple offers on a home, sellers tend to give preference to borrowers with conventional financing,” Yates said. Why is that? Sellers worry that if they accept an offer from a borrower with FHA financing, they’ll run into problems during both the home appraisal and home inspection processes.

Can you buy a fixer upper with a conventional loan?

You can certainly buy a fixer-upper with a conventional loan, and many people do, but you’ll still need a plan on how you’ll finance the renovations. … This loan type allows you to combine both the purchase and renovation of the property into one long-term, fixed-rate mortgage.

What is the maximum debt-to-income ratio for a conventional mortgage?

The maximum debt-to-income ratio (DTI) for a conventional loan is 45%. Exceptions can be made for DTIs as high as 50% with strong compensating factors like a high credit score and/or lots of cash reserves.

Are conventional loans backed by the government?

A conventional loan is a mortgage loan that’s not backed by a government agency. … Conforming conventional loans follow lending rules set by the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac).

What percentage of loans are conventional?

Conventional Loans Are 64% Of Mortgage Market.

How long do you pay mortgage insurance on a conventional loan?

That means you will have to wait at least two years before being able to get rid of your mortgage insurance. Check current mortgage rates.

Is PMI tax deductible?

The tax deduction for PMI was set to expire in the 2020 tax year, but recently, legislation passed The Consolidated Appropriations Act, 2021 effectively extending your ability to claim PMI tax deductions for the 2021 tax period. In short, yes, PMI tax is deductible for 2021.

How can I avoid closing costs?

- Look for a loyalty program. Some banks offer help with their closing costs for buyers if they use the bank to finance their purchase. …

- Close at the end the month. …

- Get the seller to pay. …

- Wrap the closing costs into the loan. …

- Join the army. …

- Join a union. …

- Apply for an FHA loan.

How do you get closing costs waived?

- Break down your loan estimate form. …

- Don’t overlook lender fees. …

- Understand what the seller pays for. …

- Think about a no-closing-cost option. …

- Look for grants and other help. …

- Try to close at the end of the month. …

- Ask about discounts and rebates.

Do closing costs come out of pocket?

How much are closing costs? Average closing costs for the buyer run between about 2% and 5% of the loan amount. That means, on a $300,000 home purchase, you would pay from $6,000 to $15,000 in closing costs. The most cost-effective way to cover your closing costs is to pay them out-of-pocket as a one-time expense.

How much is closing costs on a 200k house?

Closing costs can make up about 3% – 6% of the price of the home. This means that if you take out a mortgage worth $200,000, you can expect closing costs to be about $6,000 – $12,000. Closing costs don’t include your down payment.

Why is my closing costs so high?

So, in most cases, sellers pay as much and maybe more than buyers. Closing costs are paid in cash at the time of closing. You’ll pay higher closing costs if you choose to buy discount points and – also referred to as prepaid interest points or mortgage points, but the trade-off is a lower interest rate on your loan.