Is a home equity loan a good idea

HELOCs can come with a minimum withdrawal amount.There can be limitations to how you access the funds.There is a set withdraw period after which you cannot access any further funds.There can be fees associated with a HELOC.You can hurt your credit if you do not make payments on time.Harder to qualify right now.

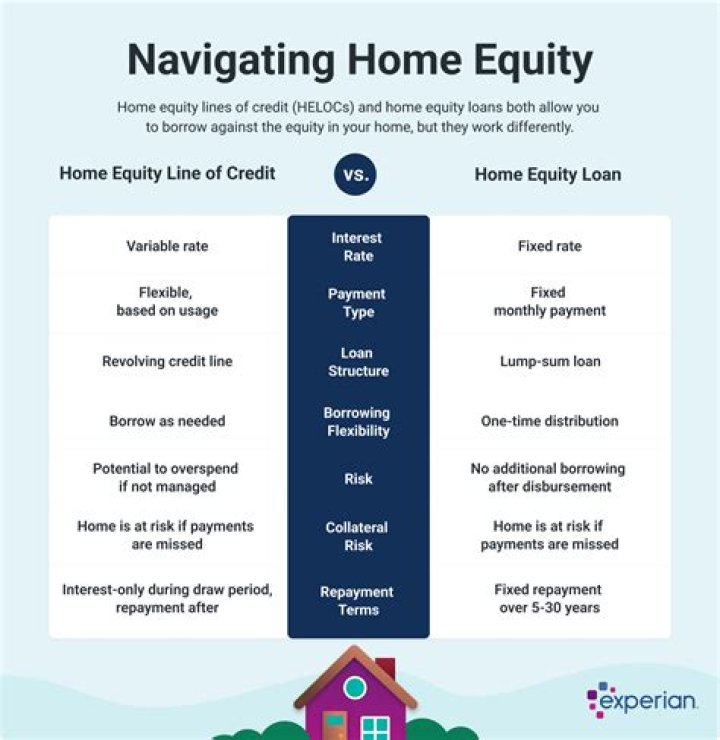

What are the disadvantages of a home equity line of credit?

- HELOCs can come with a minimum withdrawal amount.

- There can be limitations to how you access the funds.

- There is a set withdraw period after which you cannot access any further funds.

- There can be fees associated with a HELOC.

- You can hurt your credit if you do not make payments on time.

- Harder to qualify right now.

How long do you get to pay off a home equity loan?

How long do you have to repay a home equity loan? You’ll make fixed monthly payments until the loan is paid off. Most terms range from five to 20 years, but you can take as long as 30 years to pay back a home equity loan.

What is not a good use of a home equity loan?

A home equity loan could be a good idea if you use the funds to make improvements on your home or consolidate debt with a lower interest rate. However, a home equity loan is a bad idea if it will overburden your finances or if it only serves to shift debt around.What scenario do most homeowners use the equity in their home?

Homeowners sometimes use home equity to pay off other personal debts, such as car loans or credit cards. “This is another very popular use of home equity, as one is often able to consolidate debt at a much lower rate over a longer-term and reduce their monthly expenses significantly,” Hackett says.

Which one of these is the most common use of equity?

Home improvement Perhaps the most frequent use of home equity is to use it to improve the home itself. This can be a very good thing, akin to using dividends from stock holdings (or interest) to re-invest and build the value of an asset.

What is the best way to pay off your mortgage?

- Make biweekly payments.

- Budget for an extra payment each year.

- Send extra money for the principal each month.

- Recast your mortgage.

- Refinance your mortgage.

- Select a flexible-term mortgage.

- Consider an adjustable-rate mortgage.

What is the payment on a 50000 home equity loan?

Loan payment example: on a $50,000 loan for 120 months at 3.80% interest rate, monthly payments would be $501.49.Which one is the most common use of equity?

- Pay for home improvements. …

- Pay off credit cards or other higher interest debt. …

- Pay for education. …

- Fund a vacation. …

- Cover medical expenses. …

- Use as a down payment for a second home. …

- Use as a down payment for rental investment property.

The rules are clear: you don’t have to repay the equity loan itself until you come to sell your property, OR at the end of your main mortgage term – whichever of these comes sooner. However, you don’t have to wait until either of these points. You can pay back the equity loan at any point you want.

Article first time published onDo you make monthly payments on a home equity loan?

Home equity loans When you get a home equity loan, your lender will pay out a single lump sum. Once you’ve received your loan, you start repaying it right away at a fixed interest rate. That means you’ll pay a set amount every month for the term of the loan, whether it’s five years or 15 years.

What can I do with equity?

You can tap into this equity when you sell your current home and move up to a larger, more expensive one. You can also use that equity to pay for major home improvements, help consolidate other debts or plan for your retirement. Not all homeowners have equity in their homes.

How do you find out how much equity is in your home?

To calculate your home’s equity, divide your current mortgage balance by your home’s market value. For example, if your current balance is $100,000 and your home’s market value is $400,000, you have 25 percent equity in the home. Using a home equity loan can be a good choice if you can afford to pay it back.

Why you shouldn't pay off your house early?

If you have no emergency fund because you put your extra money toward an early mortgage payoff, a single financial disaster could force you to take out costly loans. Or, if your mortgage hasn’t been paid off in full yet, an emergency could lead to foreclosure on your house if it means can’t pay the mortgage later.

What happens if I pay an extra $1000 a month on my mortgage?

Paying an extra $1,000 per month would save a homeowner a staggering $320,000 in interest and nearly cut the mortgage term in half. To be more precise, it’d shave nearly 12 and a half years off the loan term. The result is a home that is free and clear much faster, and tremendous savings that can rarely be beat.

How can I pay a 200k mortgage in 5 years?

Let’s say your outstanding balance is $200,000, your interest rate is 5% and you want to pay off the balance in 60 payments – five years. In Excel, the formula is PMT(interest rate/number of payments per year,total number of payments,outstanding balance). So, for this example you would type =PMT(. 05/12,60,200000).

What is the monthly payment on a $100 000 home equity loan?

Assuming principal and interest only, the monthly payment on a $100,000 loan with an APR of 3% would come out to $421.60 on a 30-year term and $690.58 on a 15-year one. Credible is here to help with your pre-approval.

What is the monthly payment on a $200 000 home equity loan?

On a $200,000, 30-year mortgage with a 4% fixed interest rate, your monthly payment would come out to $954.83 — not including taxes or insurance.

How much equity can I get in my home after 5 years?

In the first year, nearly three-quarters of your monthly $1000 mortgage payment (plus taxes and insurance) will go toward interest payments on the loan. With that loan, after five years you’ll have paid the balance down to about $182,000 – or $18,000 in equity.

Can you sell a house that has equity release?

Many standard equity release schemes allow you to move your mortgage to a new property if you decide to sell your house, provided the lender approves the property first. … In this situation, you may have to repay some of the mortgage early, potentially triggering early repayment charges.

Do you pay interest on equity?

Accessing equity is done via increasing how much you owe. It is still a loan with interest charged for using the funds. At the moment, you may be able to afford your current repayments, however, if you increase your home loan your repayments will increase.

How fast does a home build equity?

Because so much of your monthly payments go to interest at the beginning of the loan term, it often takes about five to seven years to really begin paying down principal. Plus, it usually takes four to five years for your home to increase in value enough to make it worth selling.

How do I know if I have 20% equity in my home?

In order to pay for the rest, you got a loan from a mortgage lender. This means that from the start of your purchase, you have 20 percent equity in the home’s value. The formula to see equity is your home’s worth ($200,000) minus your down payment (20 percent of $200,000 which is $40,000).

What builds equity in a home?

You gain equity primarily from paying down the principal balance of the home loan through your monthly mortgage payments, or by an increase in your home’s market value. Check out our guide for calculating home equity easily.

Do millionaires pay off their house?

Of course there are a host of other factors, like income level and spending patterns, contributing to someone’s ability to become a millionaire, but according to Hogan’s research, the average millionaire paid off their house in 11 years and 67% live in homes with paid-off mortgages.

Is it better to have a mortgage or pay it off?

Paying off your mortgage early helps you save money in the long run, but it isn’t for everyone. Paying off your mortgage early is a good way to free up monthly cashflow and pay less in interest. But you’ll lose your mortgage interest tax deduction, and you’d probably earn more by investing instead.

What to do after you pay off your house?

- Get a Satisfaction of Mortgage Statement. …

- File the Satisfaction of Mortgage Statement With your county clerk. …

- Cancel automatic mortgage payments. …

- Notify your homeowner insurance provider. …

- Contact your local taxing authority. …

- Inquire about your escrow balance. …

- Check your credit report.