Is conforming the same as FHA

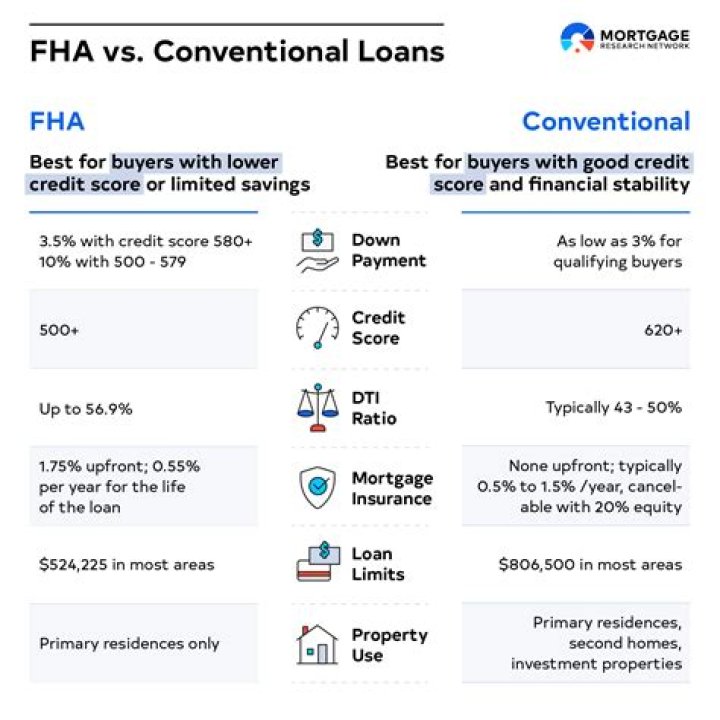

The conforming loan issues we’ve been discussing apply to conventional loans, but similar considerations apply for FHA mortgages. FHA home loans have limits that are set by county just like the Fannie and Freddie conforming loan limits. An FHA conforming loan would be at or under the FHA loan limit for that area.

Is conforming loan FHA or conventional?

Conventional loans are also called conforming loans because they conform to Fannie Mae and Freddie Mac standards. Fannie Mae and Freddie Mac are government-created enterprises that buy mortgages from lenders and hold the mortgages or turn them into mortgage-backed securities.

Are conforming and conventional loans the same?

So in this context, the term “conventional” basically means a normal or regular loan that does not receive government backing. A conforming loan is a conventional mortgage product that meets or “conforms” to certain size limits and other parameters.

Are FHA loans non-conforming?

Non-conforming loans commonly include jumbo loans (those above Fannie Mae and Freddie Mac limits) and government-backed loans like VA loans, FHA loans or USDA loans.Do I qualify for conforming loan?

To qualify for a conforming loan, you’ll generally need a credit score of at least 620, a DTI below 50% and a maximum LTV of 97% (meaning you’ll need to put at least 3% down). All these factors are interdependent, so the exact requirements for a loan will depend on your individual application.

What is a conforming loan limit?

The conforming loan limit is the dollar cap set each year for mortgages that Fannie Mae and Freddie Mac will buy or guarantee. … Mortgages that fall under the conforming loan limit are considered conforming loans, and loans that exceed the limit are called jumbo loans.

Is a conforming loan better than a conventional loan?

One common option, which is a good one for many borrowers, is a conforming loan. … They establish standard rules to qualify for a mortgage, how much you can borrow, and how your loan will be structured. You also benefit because the interest rate on conforming loans is often lower than the rate on nonconforming loans.

What type of loan is a conforming?

A conforming loan is a mortgage that meets the dollar limits set by the Federal Housing Finance Agency (FHFA) and the funding criteria of Freddie Mac and Fannie Mae. For borrowers with excellent credit, conforming loans are advantageous due to their low interest rates.What does conforming loan limits mean?

The conforming loan limit is the dollar cap on the size of a mortgage that the Federal National Mortgage Association (known colloquially as Fannie Mae) and the Federal Home Loan Mortgage Corp. … Mortgages that meet the criteria for backing by the two quasi-government agencies are known as conforming loans.

What does 30 year fixed rate conforming mean?A “fixed-rate” mortgage comes with an interest rate that won’t change for the life of your home loan. A “conventional” (conforming) mortgage is a loan that conforms to established guidelines for the size of the loan and your financial situation. … Terms of these conventional loans typically range from 10 to 30 years.

Article first time published onWhat is the FHA conforming loan limit?

The national conforming loan limit for 2022 is $647,200. FHA’s 2022 minimum national loan limit “floor”, of $420,680 is set at 65 percent of the national conforming loan limit. This “floor” applies to those areas where 115 percent of the median home price is less than the “floor” limit.

What is the minimum down payment for a conforming loan?

Conventional loan down payment requirements The minimum down payment required for a conventional mortgage is 3%, but borrowers with lower credit scores or higher debt-to-income ratios may be required to put down more.

How much is a conforming mortgage?

The baseline conforming loan limit for 2021 is $548,250 – up from $510,400 in 2020. The limit is higher in areas where the median house cost exceeds this number, so borrowers in high-cost areas can get conforming loans of up to $822,375, depending on the limit in their individual county.

What is a conforming loan vs Jumbo?

Jumbo loans live up to their name by offering a limit much higher than that placed on conforming loans. While conforming loans are created for the average homebuyer, jumbo loans are designed for high-income earners looking to purchase more expensive properties.

Will the conforming loan limit increase in 2021?

Conforming Loan Limits Increase By 18% in 2021 for the Year Ahead.

What is a FHA bond conforming fixed 30 year?

The fixed interest rate applied to this loan type implies that borrowers can expect to pay the same annual interest rate on their principal throughout the life of the mortgage, which lasts 30 years.

What are the conforming loan limits for 2020?

California Conforming Loan Limits, 2020 The California Conforming loan Limit in 2020 was $510,400 and in some high-cost counties, like Los Angeles, Orange, San Mateo, and Alameda) it was as high as $765,600.

Why are jumbo rates lower than conforming?

One of the reasons that the jumbo-to-conforming rate difference has declined is the increase in guarantee fees (also known as g-fees) for the loans bought by Fannie Mae and Freddie Mac for conforming and high-balance conforming loans. … Another reason is the comparatively higher credit standard of jumbo loans.

What will conforming loan limits be in 2022?

In 2022, you can borrow up to $647,200 with a conforming loan in most parts of the US. In areas with a higher cost of living, you may be able to borrow up to $970,800.

Will banks make loans beyond the conforming limit?

If you go beyond the conforming loan limit in your area, then you‘ll have to apply for a jumbo mortgage, which usually has stricter credit and income requirements. In addition to a higher credit score, jumbo mortgage lenders may: Ask for a larger down payment.

What is conforming home loan?

Conforming loans are loans that meet the guidelines to be purchased by government-sponsored enterprises Fannie Mae and Freddie Mac. Conforming loan limits are uniform for most states but higher in high-cost areas.

What does conforming fixed mean?

When your loan amount meets federal guidelines for conventional financing, your loan is considered “conforming.” If your loan’s interest rate will not change at any time during the repayment term, it’s consider “fixed.” Conforming fixed loans are common mortgage programs. …

What is the difference between a 30 year fixed and a 30 year FHA?

The FHA offers a 30–year fixed rate mortgage. So does Fannie Mae and Freddie Mac. However, people tend to assume that these mortgages are alike; that a 30–year fixed is a 30–year fixed is a 30–year fixed. … Conforming mortgage insurance lasts until there’s 20% equity in the home.

What is the most FHA will loan?

Generally, the most you can borrow with an FHA loan is $420,680. That applies to single–family homes, with limits increasing for 2–, 3–, and 4–unit properties and in higher–cost counties. The maximum FHA loan amount for a 1–unit property in a high–cost area is $970,800. And for a 4–unit home, it’s nearly $2 million.

Will FHA loan limits go up in 2021?

In high cost areas the FHA loan limit goes from $765,600 to $822,375 – that is an increase of over $55,000. This increase will allow California homeowners new opportunities and should help keep housing stable. All-time low mortgage rates in 2020 helped home sales and that looks to continue into 2021.

What is the down payment for FHA loan?

FHA loans have lower credit and down payment requirements for qualified homebuyers. For instance, the minimum required down payment for an FHA loan is only 3.5% of the purchase price.

What's the lowest credit score for a conventional loan?

Conventional Loans A conventional loan is a mortgage that’s not insured by a government agency. Most conventional loans are backed by mortgage companies Fannie Mae and Freddie Mac. Fannie Mae says that conventional loans typically require a minimum credit score of 620.

Can I get a mortgage with 50 DTI?

A DTI of 50% or less will give you the most options when you’re trying to qualify for a mortgage. You can use Rocket Mortgage® to see what purchase options you’re eligible for based on your DTI, credit and other factors.

Can I switch from FHA to conventional before closing?

To convert an FHA loan to a conventional home loan, you will need to refinance your current mortgage. The FHA must approve the refinance, even though you are moving to a non-FHA-insured lender. The process is remarkably similar to a traditional refinance, although there are some additional considerations.