Is FHA or conventional loan better for seller

There are two situations when a seller should choose a Conventional offer over an FHA offer. First, if the property has safety issues or things that need to be fixed, a Conventional appraisal will be less likely to point out those issues while an FHA appraiser will require those to be fixed prior to closing.

Why are FHA loans bad for sellers?

Unfortunately, some home sellers see the FHA loan as a riskier loan than a conventional loan because of its requirements. The loan’s more lenient financial requirements may create a negative perception of the borrower. And, on the other hand, the stringent appraisal requirements of the loan may make the seller nervous.

Is FHA loan good for seller?

FHA loans attract buyers who might not have the cash savings for the closing costs out of pocket. FHA loans let the seller pick up as much as 6 percent of the value of the home to pay the buyer’s closing costs, making it easier for the buyer to afford the house.

Which loans do sellers prefer?

Home sellers may prefer conventional loans because FHA loans require an FHA appraisal. Sellers are required to address any issues that come up during the appraisal — which is similar to, but not the same as, a home inspection — before closing. Some sellers don’t want to deal with this extra step and added uncertainty.Are FHA loans difficult for sellers?

FHA loans require that the home be appraised by an appraiser who meets high qualifications. The property condition is one of the biggest reasons why an FHA mortgage could be a problem for a home seller. These appraisers are looking to make sure that the house is in good condition, safe and habitable.

How much does FHA allow for seller concessions?

Seller concessions are limited to six percent of the sale price of the home and while the concessions can be used to pay some of a borrower’s closing costs, these funds can never be used as a down payment for an FHA mortgage.

Why do sellers choose conventional over FHA?

There are two situations when a seller should choose a Conventional offer over an FHA offer. First, if the property has safety issues or things that need to be fixed, a Conventional appraisal will be less likely to point out those issues while an FHA appraiser will require those to be fixed prior to closing.

Why are FHA appraisals lower than conventional?

This is because almost every mortgage has a requirement for property appraisal before the loan is given to the buyer. … The FHA loan has a minimum down payment requirement but conventional loan has a higher down payment requirement despite its lower standards.What are the pros and cons of a conventional loan?

- Credit Considerations. Riskier than mortgages backed by the US government, conventional loans typically hold borrowers to a higher standard. …

- Money Down & Mortgage Insurance. …

- More Options. …

- Time & Cost to Close. …

- A Seller’s Market.

Some agents advise home sellers to take conventional loan or cash offers, even if they are lower than VA offers, because those options are perceived as less hassle than VA loans. … “Choosing a conventional offer over a VA offer is not considered discrimination.”

Article first time published onWhat is the minimum down payment for a conventional loan?

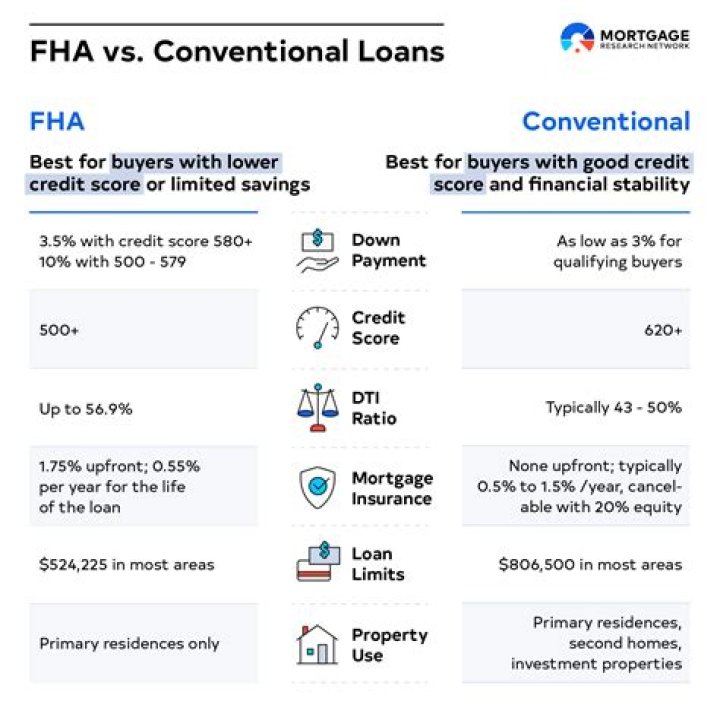

The minimum down payment required for a conventional mortgage is 3%, but borrowers with lower credit scores or higher debt-to-income ratios may be required to put down more.

Why would a seller require a conventional loan?

Length of Time to Close. By and large, conventional loans simply tend to close faster. Less paperwork and fewer stipulations allow these mortgages to be processed more quickly, and many sellers find this to be an attractive bonus.

Does Fannie Mae back conventional loans?

Fannie Mae is a government-sponsored enterprise that makes mortgages available to low- and moderate-income borrowers. It does not provide loans, but backs or guarantees them in the secondary mortgage market.

Is it hard to get a conventional home loan?

Even though a conventional loan is the most common mortgage, it is surprisingly difficult to get. Borrowers need to have a minimum credit score of about 640 in order to qualify—the highest minimum score of all mortgage products—and have a debt-to-income ratio of 43% or less.

What is the maximum seller credit on a conventional loan?

The limit for conventional loans depends on how much you’re putting down: If your down payment is less than 10%, the seller can contribute up to 3%. If your down payment is 10% – 25%, the seller can contribute up to 6%. If your down payment is more than 25%, the seller can contribute up to 9%.

Can seller pay closing costs on conventional loan?

Conventional loans Conventional loan guidelines are a little more restrictive than other types of loans. Depending on the buyer’s loan-to-value (LTV) ratio and downpayment, a seller can contribute anywhere from 3% to 9% of the sales price in closing costs.

What does seller pay for at closing?

Seller concessions are closing costs that the seller agrees to pay and can substantially reduce the amount of cash you need to bring on closing day. Sellers can agree to help pay for things like property taxes, attorney fees, appraisal inspections and mortgage discount points to lower your interest rate.

What is the downside of a conventional loan?

A disadvantage to conventional lending is generally lower debt-to-income ratios are required. Low income and high debt scenarios pose additional risk to private lenders, therefore debt ratio requirements are more stringent with conventional loans.

What is bad about conventional loan?

Conventional loans often require a credit score of at least 620, which leaves out some homebuyers. Even if you qualify, you will likely pay a higher interest rate than if you had good credit. More stringent DTI requirements. Conventional loans typically demand higher DTIs than government programs do.

Can I put 3 down on a conventional loan?

Can I get a mortgage with 3% down? Yes! The conventional 97 program allows 3% down and is offered by many lenders. Fannie Mae’s HomeReady loan and Freddie Mac’s Home Possible loan also allow 3% down with extra flexibility for income and credit qualification.

Can you switch from FHA to conventional?

To convert an FHA loan to a conventional home loan, you will need to refinance your current mortgage. The FHA must approve the refinance, even though you are moving to a non-FHA-insured lender. The process is remarkably similar to a traditional refinance, although there are some additional considerations.

What will fail an FHA appraisal?

This means severe structural damage, leakage, dampness, decay or termite damage can cause the property to fail inspection. In such a case, repairs must be made in order for the FHA loan to move forward.

Are appliances required for a conventional loan?

A fully functional kitchen with appropriate appliances (i.e., sink, cabinets, utilities to support a stove and refrigerator). Stove and refrigerator do not need to be present if they are not a built-in, as non-built in appliances are considered personal property. Comparables without appliances are not required.

Why do Realtors hate VA loans?

Many sellers – and their real estate agents – don’t like VA loans because they believe these mortgages make it harder to close or more expensive for the seller. … Are less likely to close than other types of mortgages. Take ages to reach closing. Have appraisers who are slow and routinely undervalue homes.

Why are sellers afraid of VA loans?

Before it guarantees mortgages, the VA wants to ensure homes that eligible veterans buy are safe and secure as well as worth their sale price. … Because VA appraisals may increase their repair costs, home sellers sometimes refuse to accept purchase offers backed by the agency’s mortgages.

Is a VA loan bad for the seller?

Using a VA loan means you’ll end up saving money both on the purchase and over the life of the loan. However, it does mean the person selling you the house will have to spend more to sell you the house. If you’re worried about the seller denying your offer because you’re using a VA loan, don’t be.

Can you put 5% down on a conventional loan?

Downpayment for Conventional Loans: 5% Conventional loans require buyers to make a minimum 5 percent downpayment on a home. Because this is a conventional loan, and because the downpayment is less than twenty percent, private mortgage insurance (PMI) will be required.

Do conventional loans require PMI?

If you put down less than 20% on a conventional loan, you’ll be required to pay for private mortgage insurance (PMI). PMI protects your lender in case you default on your loan. The cost for PMI varies based on your loan type, your credit score and the size of your down payment.

Can you buy a fixer upper with a conventional loan?

You can certainly buy a fixer-upper with a conventional loan, and many people do, but you’ll still need a plan on how you’ll finance the renovations. … This loan type allows you to combine both the purchase and renovation of the property into one long-term, fixed-rate mortgage.

Why would a house be cash or conventional only?

Some sellers will have their home listed on the market allowing only a Cash or Conventional loan buyer to make offers on it. … The usual reason for this is because the appraisal done on an FHA or VA loan is a little more stringent with it’s requirements for the property to meet the government FHA or VA standards.

Why did my mortgage get sold to Fannie Mae?

Fannie Mae buys mortgage loans from lenders to replenish their funds so the lenders can continue making new mortgage loans. That helps keep affordable financing available for homebuyers in the market for a home.