What are Reg Z fees

Section 1026.4(a) of Regulation Z defines a finance charge as “the cost of consumer credit as a dollar amount. It includes any charge payable directly or indirectly by the consumer and imposed directly or indirectly by the creditor as an incident to or a condition of the extension of credit.

What does Regulation Z mean?

Regulation Z is a law that protects consumers from predatory lending practices. Also known as the Truth in Lending Act, the law requires lenders to disclose borrowing costs so consumers can make informed choices.

Which transaction is not covered by Regulation Z?

Regulation Z does not apply, except for the rules of issuance of and unauthorized use liability for credit cards. (Exempt credit includes loans with a business or agricultural purpose, and certain student loans.

What is Regulation Z and what does it cover?

Regulation Z is a federal law that standardizes how lenders convey the cost of borrowing to consumers. It also restricts certain lending practices and protects consumers from misleading lending practices.What fees are included in the finance charge?

A finance charge is the total amount of interest and loan charges you would pay over the entire life of the mortgage loan. This assumes that you keep the loan through the full term until it matures (when the last payment needs to be paid) and includes all pre-paid loan charges.

What triggers Regulation Z?

Payment information in an advertisement is also a triggering term requiring additional disclosures. … Regulation Z prohibits misleading terms in open-end credit advertisements.

What is Regulation Z and TILA?

TILA promotes the informed use of consumer credit by requiring timely disclosure about its costs. It also includes substantive provisions such as the consumer’s right of rescission on certain mortgage loans and timely resolution of billing disputes.

What is Reg Z section 32?

Section 32 of Regulation Z implements the Home Ownership and Equity Protection Act of 1994 (HOEPA). HOEPA protects consumers from deceptive and unfair practices in home equity lending by establishing specific disclosure requirements for certain mortgages that have high rates of interest or assess high fees and points.What is Regulation Z credit card?

Regulation Z generally prohibits a card issuer from opening a credit card account for a consumer, or increasing the credit limit applicable to a credit card account, unless the card issuer considers the consumer’s ability to make the required payments under the terms of such account.

What is an example of prohibited compensation?Prohibited compensation practices; Regulatory Tip: Only the provisions on mandatory arbitration, waivers of federal claims, and financing credit insurance premiums apply to HELOCs secured by a member’s principal dwelling. Restricted financing of credit insurance premiums.

Article first time published onWhat are the two most important disclosures that appear on the Reg Z disclosure statement?

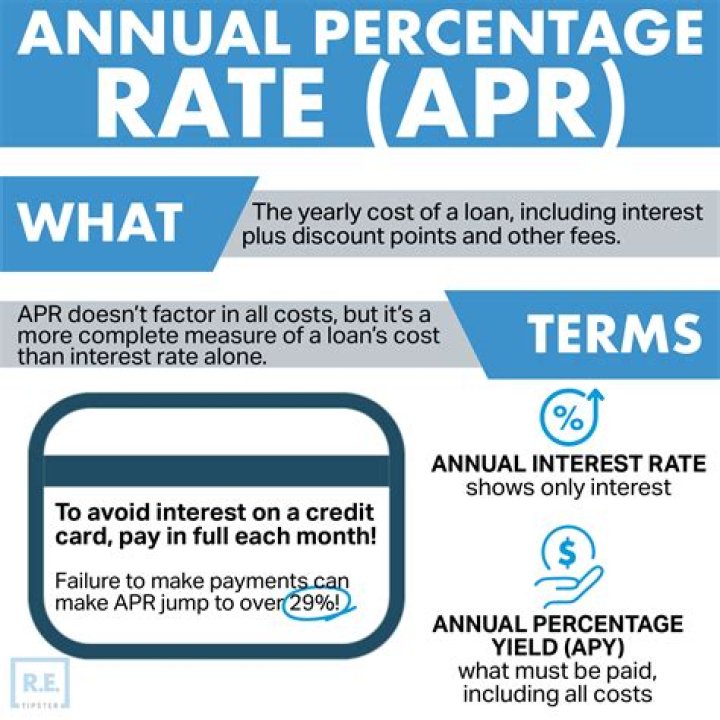

Reg Z requires disclosure of the finance charge and Annual Percentage Rate (APR) regardless of whether you are granting a revolving credit line or an installment loan. days after approval to give the applicant time to decide whether or not to accept.

Who enforces Regulation Z?

The FTC enforces TILA and its implementing Regulation Z with regard to most non- bank entities. policy development; and consumer and business education (all relating to the topics covered by Regulation Z, including the advertisement, extension, and certain other aspects of consumer credit).

What is the tolerance for APR disclosure for a foreclosure?

That section incorporates the statutory APR tolerances of 1/8 of 1 percent for regular transactions and ¼ of 1 percent for irregular transactions. Under the statutory tolerances, the disclosed APR is deemed to be accurate if it is above or below the actual APR by no more than the applicable percentage.

What fees are not included in Apr?

- Title or abstract fee.

- Attorney fee.

- Notary fee.

- Document preparation (charged by the closing agent)

- Home-inspection fees.

- Recording fee.

- Transfer taxes.

- Credit report.

What fees are excluded from finance charges?

Charges Excluded from Finance Charge: 1) application fees charged to all applicants, regardless of credit approval; 2) charges for late payments, exceeding credit limits, or for delinquency or default; 3) fees charged for participation in a credit plan; 4) seller’s points; 5) real estate-related fees: a) title …

What fees affect the APR?

- Discount points.

- Mortgage broker fees.

- Transaction fees.

- Mortgage insurance.

- Application and processing fees.

- Legal fees.

- Origination fees.

- Mortgage underwriter fees.

Are HELOCs subject to Reg Z?

HELOCs are interesting, as they are open-end lines of credit governed by Subpart B of Reg Z, but also have their own rules under section 1026.40.

What does MSA stand for in mortgage?

Marketing Services Agreements (MSAs) have been part of the mortgage landscape for two decades, they are financial arrangements between compensated real estate (or real estate universe) entities and compensating mortgage lenders.

What is covered by Reg B?

Regulation B covers the actions of a creditor before, during, and after a credit transaction. … This list also includes refinancing, credit applications, information requirements, standards of creditworthiness, investigation procedures, and revocation or termination of credit.

Why would a mortgage beneficiary have an appraisal on the property?

Appraisals are third-party valuations of a property based on a wide range of variables. Lenders generally insist on this independent assessment to make sure the value of the property is at least sufficient to pay off the loan amount in case of default. In a repayment of a mortgage loan, which type of interest is used?

Is zero down payment a trigger term?

Answer: Unless you are involved in advertising a credit sale (i.e., you are financing property you are selling), any mention of a downpayment amount or percentage is not a trigger term.

Is no closing costs a trigger term?

Statements of the annual percentage rate or statements that there is no particular charge for credit (such as “no closing costs”) are not triggering terms under this paragraph.

What is the difference between ECOA and Regulation B?

What is the difference between the ECOA and Regulation B? The ECOA is the Equal Credit Opportunity Act, which Congress passed to prohibit lending discrimination on the basis of certain factors. Regulation B is the rule that the Federal Reserve created to enforce the ECOA.

What fees are included in high-cost test?

Points and Fees Test A mortgage is also considered to be a high-cost mortgage if its points and fees exceed: 5% of the total loan amount if the loan amount is equal to or more than $22,052 (2021), or. 8% of the total loan amount or $1,103 (whichever is less) if the loan amount is less than $22,052.

Does high-cost apply to investment properties?

The Home Ownership and Equity Protection Act (HOEPA) of 1994 defines high-cost mortgages. … It covers certain mortgage transactions that involve the borrower’s primary residence. The law does not apply to mortgage transactions that involve investment properties, commercial real estate or real estate purchases.

What makes a mortgage loan high-cost?

Under the new rule, a mortgage will be considered high-cost if it is: A first mortgage with an annual percentage rate (APR) that is more than 6.5 percentage points higher than the average prime offer rate. … A loan of $20,000 or more with points and fees that exceed 5 percent of the loan amount.

Which of the following fees would be prohibited under respa Section 8?

Section 8: Kickbacks, Fee-Splitting, Unearned Fees In addition, RESPA prohibits fee splitting and receiving unearned fees for services not actually performed. Violations of Section 8’s anti-kickback, referral fees and unearned fees provisions of RESPA are subject to criminal and civil penalties.

Does the CFPB prohibit compensation based off of commission?

Prohibition Against Dual Compensation. The final rules implement the codification of this prohibition in the Act and add an exception for mortgage brokers that pay their employees or contractors commissions, although the commission cannot be based on the loan’s terms.

What is the 3 7 3 mortgage rule?

1. The 3/7/3 Rule requires a seven business day waiting period once the initial disclosure is provided before closing a home loan (business days are everyday except Sundays and Holidays).

Is an application fee a finance charge?

1. Application fees. An application fee that is excluded from the finance charge is a charge to recover the costs associated with processing applications for credit. The fee may cover the costs of services such as credit reports, credit investigations, and appraisals.

What are the penalties for violating Tila?

Criminal penalties – Willful and knowing violations of TILA permit imposition of a fine of $5,000, imprisonment for up to one year, or both.