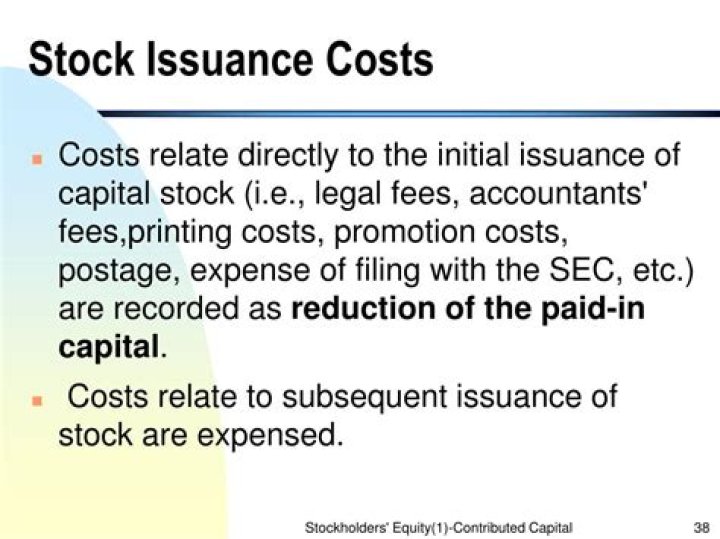

What are stock issuance costs

Definition. The financial accounting term stock issuance costs refers to the expenses a corporation incurs when they issue securities to the market. Typical costs associated with issuing stock include fees for attorneys, accountants, as well as underwriting.

Is share issuance cost will be categorized as expense?

Costs that relate to the stock market listing, or are otherwise not incremental and directly attributable to issuing new shares, should be recorded as an expense in the statement of comprehensive income.

Are stock issuance costs amortized?

BOOK TREATMENT: Stock issuance costs should be considered a reduction of the related proceeds and recorded net with the amount received in equity. These costs are not amortized.

Are stock issuance costs capitalized?

There are two ways in which these stock issuance costs can be accounted for under GAAP. Treat the issue costs as a reduction of the amounts paid in. … Capitalize the amount as an organizational cost on the balance sheet and amortize the this intangible asset similarly to the amortization of goodwill.How is equity issuance cost treated?

Accounting for Issuance Fees Equity issuance fees may be listed as a reduction of paid-in capital. The reduction is taken from paid-in capital (the amount paid by investors during common or preferred stock issuance) that exceeds the par value. It is a static value of the security.

What are some of the costs associated with the issuance of new shares of stock?

There are flotation costs associated with issuing new equity, or newly issued common stock. These include costs such as investment banking and legal fees, accounting and audit fees, and fees paid to a stock exchange to list the company’s shares.

What is an issuance in accounting?

What Is an Issue? An issue is a process of offering securities in order to raise funds from investors. Companies may issue bonds or stocks to investors as a method of financing the business.

What is equity issuance discount?

Definition: A discount on stock occurs when the stock’s par value is higher than the issuing price. The difference between the greater par value and the lesser issue price is considered the discount. This represents the amount of the par value that investors were unwilling to pay for when the stock was issued.Are IPO costs tax deductible?

CONCLUSION. No, a taxpayer may not deduct under section 165 previously capitalized costs that facilitated an IPO when the taxpayer later ceases to be a publicly traded company as a result of a take private transaction. The costs are capitalized via netting against the proceeds, so there is no amount to later recover.

What are debt issuance costs?Debt issuance costs are those associated with issuing loans and bonds, such as fees and commissions paid to investment banks, law firms, auditors and regulators. … Debt issuance costs are presented as a deferred asset, while any discounts or premiums are netted with the debt liability.

Article first time published onWhat is Bond issuance cost?

Bond issue costs are the fees associated with the issuance of bonds by an issuer to investors. … These costs are recorded as a deduction from the bond liability on the balance sheet. The costs are then charged to expense over the life of the associated bond, using the straight-line method.

Can you capitalize M&A fees?

Associated transaction costs incurred related to a merger or acquisition transaction can be significant. … Generally, costs that facilitate a transaction must be capitalized. These costs include amounts paid in the process of investigating or otherwise pursuing the transaction.

Are capital raising costs tax deductible?

Certain start-up expenses, including costs associated with raising capital, that would otherwise be deductible over five years are immediately deductible (from July 1, 2015) where they are incurred by an SBE or an entity that is not in business.

How do I account for M&A fees?

- Identify a business combination.

- Identify the acquirer.

- Measure the cost of the transaction.

- Allocate the cost of a business combination to the identifiable net assets acquired and goodwill.

- Account for goodwill.

When cash is received from a stockholder in exchange for common stock?

The general journal entry to record this transaction will be: Debit Cash, credit Services Revenue. When cash is received from a stockholder in exchange for common stock, the transaction is recorded by debiting Cash and crediting a(n. Equity account.

What is issuance of common stock on financial statement?

The initial issuance of common stock reflects the sale of the first stock by a corporation. Common stock issued at par value for cash creates an additional paid-in capital account for the excess of the issue price over the par value.

Which is the most expensive source of fund?

The most expensive source of capital is usually: b. new common stock. Companies can use various sources of capital for their business.

Does issuance of common stock increase stockholders equity?

The effect on the Stockholder’s Equity account from the issuance of shares is also an increase. Money you receive from issuing stock increases the equity of the company’s stockholders. … The result equals the total amount you receive from the stock issuance, and the total increase to the Stockholder’s Equity account.

Does issuance of stock increase stockholders equity?

While issuing new stock can increase stockholders’ equity, stock splits do not have the same impact. … Since a stock split does not bring in additional revenue for a company, it does not increase stockholders’ equity.

Is issuance of common stock a revenue?

Money an organization derives through share issuance is not revenue. The corporation makes money by selling goods or providing services, not through cash inflows from investors.

How do you calculate impact cost?

The impact cost is the percentage price movement caused by an order size of Rs. 1 Lakh from the average of the best bid and offer price in the order book snapshot. The impact cost is calculated for both, the buy and the sell side in each order book snapshot.

Are IPO costs capitalized?

Capitalization of IPO and SPAC transaction costs Capitalization of costs generally is required if the costs facilitate the merger, acquisition or stock issuance. The regulations provide additional guidance regarding what costs must be capitalized by describing the meaning of the word ‘facilitate’ in this context.

How long after an IPO can you sell?

Like any investment you make, you can sell the shares you received through IPO Access at any point in time. However, if you sell IPO shares within 30 days of the IPO, it’s considered “flipping” and you may be prevented from participating in IPOs for 60 days.

How is IPO calculated?

A company’s share price at the time of the IPO is determined by the valuation of the company, divided by the total number of shares at listing. New Delhi: The listing price of an IPO (initial public offering) is decided on the basis of demand and supply of shares that aims to strike a balance between the two.

How do you know if a stock is trading at a discount?

If the price of the bond in the market is lower than $1,000, it is said to be trading at a discount. A discount bond may be contrasted with a bond trading at a premium, where the market price is above its face.

What is the difference between called up capital and paid up capital?

The difference between called-up share capital and paid-up share capital is that investors have already paid in full for paid-up capital. Called-up capital has not yet been completely paid, though payment has been requested by the issuing entity.

What does debt issuance mean?

A debt issue refers to a financial obligation that allows the issuer to raise funds by promising to repay the lender at a certain point in the future and in accordance with the terms of the contract. A debt issue is a fixed corporate or government obligation such as a bond or debenture.

How do you handle debt issuance cost?

To account for the expenses associated with bond issuance, debit the debt issuance costs account and credit the accounts payable account to account for the associated liability. Since the debt issuance account is an asset account, the issuance costs will first be recorded in the balance sheet of the bond issuer.

Where do debt issuance costs go on the cash flow?

Debt-issuance costs go on the cash flow statement through the income statement as expenses and also through the balance sheet as changes to cash assets. The proceeds from the debt issues go on the financing-activities section of the cash flow statement, but the issuance costs go on the operating-activities section.

Are debt issuance costs subject to 163 J?

163(j) business interest expense limitation was the reworked definition of “interest,” which now does not include debt issuance costs or commitment fees (T.D. 9905). … This change to the definition of interest is generally taxpayer-favorable, because it means these loan fees do not count toward the Sec.

Are promotion costs bond issuance costs?

expenditures incurred in preparing and selling a bond issue such as legal, underwriting, accounting, commission, printing, promotion, and registration fees. Note that the amortization starts from the date the bonds are sold and notthe date of the bonds (which may be before the issue date). …