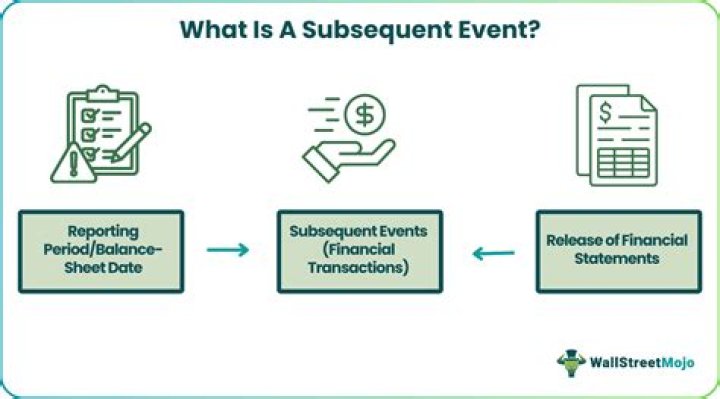

What are the subsequent events

A subsequent event is an event that occurs after a reporting period, but before the financial statements for that period have been issued or are available to be issued. Depending on the situation, such events may or may not require disclosure in an organization’s financial statements.

What are Type 1 and Type 2 subsequent events?

Type I subsequent events provide evidence about conditions that existed on or before the balance sheet date. These events are recognized in the financial statements. Type II subsequent events provide evidence about conditions that did not exist on or before the balance sheet date.

What is a recognized subsequent event?

Recognized or type 1 subsequent events are typically events that occurred at the financial statement date. But that may have concluded after the year end. The financial statements must then be altered to include this event because it would be misleading not to list the event.

What is an example of a Type 1 subsequent event?

An example of a Type I subsequent event is: A tornado that destroys an entity’s factory after the balance sheet date. An event after the balance sheet date that confirms the auditor’s belief (documented prior to the end of the entity’s fiscal year) that a large portion of the entity’s inventory is obsolete.What are subsequent entries?

Subsequent event is the accounting term for a financial transaction that occurs after completion of the balance sheet for a specified period but before the company’s full set of financial statements is prepared.

Which of the following is an example of a type 2 subsequent event?

An example of a Type II subsequent event would be the bankruptcy of a client’s customer after year-end as a result of poor financial condition that existed as of the balance sheet date.

What is an adjusting event?

Adjusting event: An event after the reporting period that provides further evidence of conditions that existed at the end of the reporting period, including an event that indicates that the going concern assumption in relation to the whole or part of the enterprise is not appropriate. [

Which of the following are subsequent events that must be disclosed in the notes to the financial statements?

Which of the following is a subsequent event that must be disclosed in the notes to the financial statements? The issuance of debt or equity securities. Which of the following are required disclosures for related-party transactions?What subsequent events should be disclosed?

- Sale of a bond or capital stock issued after the balance sheet date;

- A business combination that occurs after the balance sheet date;

- Settlement of litigation when the event giving rise to the claim took place after the balance sheet date;

In this ISA, the term “subsequent events” is used to refer to both events occurring between the date of the financial statements and the date of the auditor’s report, and facts discovered after the date of the auditor’s report. 2.

Article first time published onWhat does the word subsequent?

Full Definition of subsequent : following in time, order, or place subsequent events a subsequent clause in the treaty.

What are the auditor's responsibility for subsequent events?

The overall objective of ISA 560 is to ensure the auditor performs audit procedures that are designed to obtain sufficient appropriate audit evidence to give reasonable assurance that all events up to the (expected) date of the auditor’s report have been identified, properly accounted for/r disclosed in the financial …

What are adjusting events examples?

Examples of adjusting events include: • events that indicate that the going concern assumption in relation to the whole or part of the entity is not appropriate; • settlements after reporting date of court cases that confirm the entity had a present obligation at reporting date; • receipt of information after reporting …

What is a non-adjusting subsequent event?

Non-adjusting events A subsequent event that provides new information about a condition that did not exist on the balance sheet date.

What are the non-adjusting events?

Non-adjusting events are indicative of a condition that arose after the end of the reporting period and do not result in adjustment to the financial statements. They should be disclosed if of such importance that non-disclosure would affect the ability of the users to make proper evaluations and decisions.

Which of the following is an example of a subsequent event that requires disclosure?

Examples of events of the second type that require disclosure to the financial statements (but should not result in adjustment) are: Sale of a bond or capital stock issue. Purchase of a business. Settlement of litigation when the event giving rise to the claim took place subsequent to the balance-sheet date.

What is subsequent measurement in accounting?

Subsequent measurement depends on the category of financial instrument. Some categories are measured at amortised cost, and some at fair value. … financial liabilities that are not carried at fair value through profit or loss or otherwise required to be measured in accordance with another measurement basis.

What is commonly referred to in auditing as a subsequent event?

. 10 There is a period after the balance-sheet date with which the auditor must be concerned in completing various phases of his audit. This period is known as the “subsequent period” and is considered to extend to the date of the auditor’s report.

How can management identify subsequent events?

- Enquiring into management’s procedures/systems for the identification of subsequent events;

- Inspection of minutes of members’ and directors’ meetings;

- Reviewing accounting records including budgets, forecasts and interim information.

What is the appropriate date on the auditor's report?

The auditor should date the report no earlier than the date of approval of the financial statements. This involves deciding on when the work necessary to support the opinion on the financial statements has been completed, however, the auditor may not yet have fulfilled all responsibilities related to the audit.

Which type of subsequent event requires consideration by management and evaluation by the auditor?

Which type of subsequent event requires consideration by management and evaluation by the auditor? Subsequent events that have a direct effect on the financial statements and require adjustment. Subsequent events that do not have a direct effect on the financial statements but for which disclosure may be required.

What is subsequent example?

The definition of subsequent is happening or coming after something or someone else. An example of subsequent is heavy winds that come after a hurricane has left an area. adjective. subsequent to. after; following.

What is a subsequent meeting?

A meeting of people who have the same interests, or belong to the same organization.

What is subsequent population?

adjective [ADJ n] You use subsequent to describe something that happened or existed after the time or event that has just been referred to. [formal] …the increase of population in subsequent years. Synonyms: following, later, succeeding, after More Synonyms of subsequent.

Which of the following material events occurring subsequent to the balance sheet date would require an adjustment to the financial statements before they are issued?

Which of the following material events occurring subsequent to the balance sheet date would require an adjustment to the financial statements before they could be issued? Settlement of litigation, in excess of the previously recorded liability.

What are events after the reporting period?

Events after the reporting period are those events, favourable and unfavourable, that occur between the end of the reporting period and the date when the financial statements are authorised for issue.

What is a subsequent auditor?

an individual as auditor for more than one term of five consecutive years. an audit firm as auditor for more than two terms of five consecutive years.

Which of the following are examples of non-adjusting events under IAS 10 subsequent events?

- decline in market value of investments;

- announcement of a plan to discontinue part of the enterprise;

- major purchases and sales of assets;

- destruction of a major asset by fire etc;

- sale of a major subsidiary;

- major dealings in the company’s ordinary shares;

Is a fire an adjusting or non-adjusting event?

The destruction of the plant by fire is a non-adjusting event after the end of the reporting period. The fire is a condition that arose after the end of the reporting period (see paragraph 32.2(b)). The entity does not adjust the amounts recognised in its financial statements.

Is proposed dividend an adjusting event?

after the balance sheet date” states that proposed dividend is an adjusting event. events to be disclosed in the report of the approving authority, for example, the board report.

What is frs101?

What is FRS 101? FRS 101 is essentially a reduced disclosure framework that provides reduced disclosure exemptions from EU-adopted IFRS for qualifying entities.