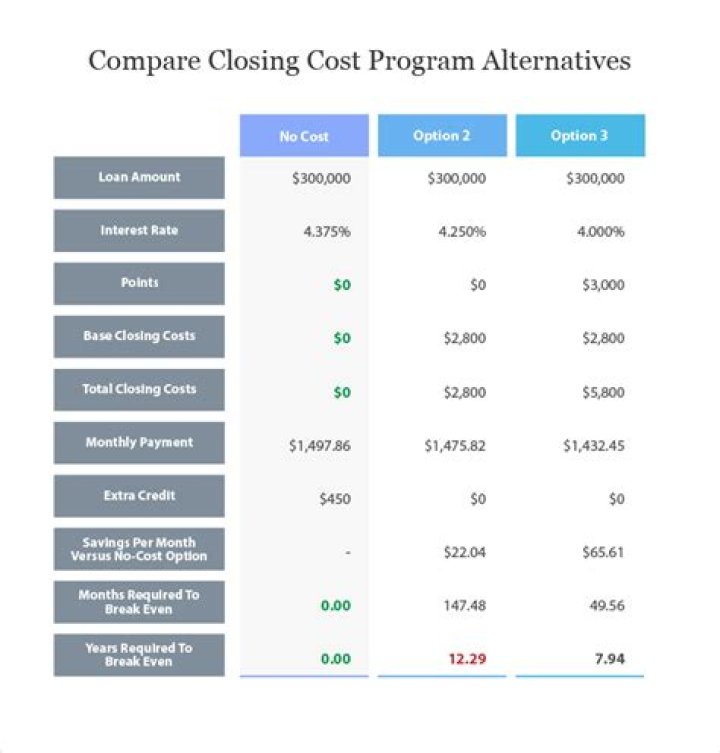

What does a no cost loan mean

A no-cost mortgage is a mortgage refinancing situation in which the lender pays the borrower’s loan settlement costs and then extends a new mortgage loan. In a no-cost mortgage, the lender covers the loan settlement costs in exchange for charging the borrower a higher interest rate on their loan.

What does a no fee mortgage mean?

A no-fee mortgage is when a lender charges no fees for a mortgage application, appraisal, underwriting, processing, private mortgage insurance and other third-party closing costs.

Does better offer no cost refinance?

You can get a personalized rate quote from Better Mortgage in minutes, without affecting your credit score. Every rate quote will provide options for paying points and taking credits, including a no-cost option. Try it and see which option is best for you.

How much should you pay in closing cost to refinance?

How refinance closing costs are determined. Average closing costs normally range from 2% to 5% of the loan amount. If you’re refinancing a $200,000 mortgage loan, for example, you could expect to pay between $4,000 and $10,000 in closing costs. This is a wide price range.What's the catch with refinancing?

The catch with refinancing comes in the form of “closing costs.” Closing costs are fees collected by mortgage lenders when you take out a loan, and they can be quite significant. Closing costs can run between 3–6 percent of the principal of your loan.

What does no point no cost mean?

No closing cost mortgages—also sometimes called no point, no fee loans—are quite popular with consumers. However, the terminology can be confusing, since these mortgages don’t eliminate costs but rather shift them from upfront costs to costs paid over time—a reality some lenders try to downplay.

Is it worth adding mortgage fee to mortgage?

If you add the fees onto your mortgage, it protects you from losing any part of the fee paid upfront if your mortgage (or property purchase) doesn’t go ahead for any reason. Don’t worry about it affecting your loan-to value band, adding it won’t.

What should you not do when refinancing?

- 1 – Not shopping around. …

- 2- Fixating on the mortgage rate. …

- 3 – Not saving enough. …

- 4 – Trying to time mortgage rates. …

- 5- Refinancing too often. …

- 6 – Not reviewing the Good Faith Estimate and other documentats. …

- 7- Cashing out too much home equity. …

- 8 – Stretching out your loan.

Are mortgage fees refundable?

A It is perfectly normal practice for certain fees paid at the time of a mortgage application not to be refunded if the mortgage does not go ahead. However, a prospective borrower should be made aware of this before paying any money for such a fee.

How can I avoid paying closing costs?- Look for a loyalty program. Some banks offer help with their closing costs for buyers if they use the bank to finance their purchase. …

- Close at the end the month. …

- Get the seller to pay. …

- Wrap the closing costs into the loan. …

- Join the army. …

- Join a union. …

- Apply for an FHA loan.

Does refinancing hurt credit?

Taking on new debt typically causes your credit score to dip, but because refinancing replaces an existing loan with another of roughly the same amount, its impact on your credit score is minimal.

Can closing costs be rolled into mortgage?

Most lenders will allow you to roll closing costs into your mortgage when refinancing. Generally, it isn’t a question of which lender that may allow you to roll closing costs into the mortgage. It’s more so about the type of loan you’re getting – purchase or refinance.

Why is my closing costs so high?

So, in most cases, sellers pay as much and maybe more than buyers. Closing costs are paid in cash at the time of closing. You’ll pay higher closing costs if you choose to buy discount points and – also referred to as prepaid interest points or mortgage points, but the trade-off is a lower interest rate on your loan.

How much does it cost to refinance a mortgage 2021?

How much does it cost to refinance a mortgage in 2021? Generally speaking, you should expect to pay anywhere from 2% to 5% of the amount of your new loan when you refinance. This means that if you’re taking out a new $200,000 mortgage, you should expect to be charged $4,000 to $10,000 in closing costs.

Should I refinance if I only have 5 years left?

The breakeven period is how long it will take you to pay off the costs of closing on a new mortgage and start realizing the savings from a lower rate and lower monthly payments. Andrews said for most people, it’s only worthwhile to refinance if your breakeven period is two years or less.

Why do lenders want you to refinance?

Your servicer wants to refinance your mortgage for two reasons: 1) to make money; and 2) to avoid you leaving their servicing portfolio for another lender. Some servicers will offer lower interest rates to entice their existing customers to refinance with them, just as you might expect.

How do you know if refinancing is worth it?

Mortgage rates have gone down So how much should mortgage rates fall before you consider whether refinancing is worth it? The traditional rule of thumb says to refinance if your rate is 1% to 2% below your current rate. Make sure to factor in your current loan term when considering refinance though.

Can you leave a fixed mortgage early?

Can you get out of a fixed rate mortgage early? Yes, it may be possible to leave your fixed rate mortgage early but (and it’s a big but) most mortgage lenders will apply an early repayment charge. … The way this charge is applied varies from lender to lender. Often, it’s a percentage of the loan, usually between 1-5%.

Are arrangement fees worth it?

However, it is only advisable to do so if you cannot afford to pay the arrangement fee straight away but the lower rate will save you more money in the long run. Adding it to your mortgage will technically increase the fee as you will pay some level of interest on the extra addition to the mortgage.

Are early repayment fees tax deductible?

So whilst the mortgage redemption fee wasn’t allowable against CGT, it should be deductible from the rental income in the year. … However, they are allowable costs against any rental income received in the tax year.

How much does 1 point lower your interest rate?

Each point typically lowers the rate by 0.25 percent, so one point would lower a mortgage rate of 4 percent to 3.75 percent for the life of the loan.

How long does Funding take after closing refinance?

You won’t receive the funds until three to five days after closing. The Truth in Lending Act requires your lender to give you three business days after closing to cancel the refinance. Since the loan isn’t technically closed until after that time passes, you won’t receive your funds until then.

Should you pay closing costs out of pocket?

How much are closing costs? Average closing costs for the buyer run between about 2% and 5% of the loan amount. That means, on a $300,000 home purchase, you would pay from $6,000 to $15,000 in closing costs. The most cost-effective way to cover your closing costs is to pay them out-of-pocket as a one-time expense.

What fees do banks charge for a mortgage?

The loan origination fee is probably the largest single closing cost you’ll encounter, as it’s the primary way lenders make money. Lenders typically charge 1% of the total loan amount for the origination fee. For example, if you take out a $100,000 mortgage, the fee would be $1,000.

What is initial term cost mortgage?

In layman’s terms, the initial term cost is the rate charged during the introductory period of a mortgage or any other loan. The rate you pay depends on the lender and can last anywhere between one month and 10 years – though initial rates between two, three and five years are far more common in the mortgage world.

Do all banks charge a mortgage application fee?

Loan application fees will vary by lender, and many lenders will not charge a loan application fee at all. … Borrowers should also seek to compare application fees across lenders. Loan application fees can vary significantly among different types of lenders, ranging on a mortgage loan anywhere from $0 to $500.

What is considered a big purchase during underwriting?

A big purchase is anything that could affect your debt-to-income ratio. … ‘ If the answer to these questions is yes, then you should hold off that big purchase until you close on the home. If you are not sure how a big purchase will affect your loan approval, don’t hesitate to speak to your loan officer beforehand.

Can I negotiate closing costs with lender?

You can work with your lender, real estate agent and seller to bring your closing costs down by comparing fees and other charges.

What lenders have the lowest closing costs?

Mortgage LenderAverage Total Loan Costs, 2020 (as % of Average Loan Amount) 2Example: Upfront Costs for $250,000 MortgageSupreme Lending0.64%$1,612Citibank0.83%$2,070PNC0.90%$2,248Chase0.99%$2,470

Are realtor fees included in closing costs?

Do closing costs include realtor fees? Yes, typically closing costs for the seller will include realtor fees.

Why did my credit score drop 40 points?

Pulling your credit report is the first step to identifying why your score dropped 40 points. You can identify all recent negative items that may have affected your score, leading to the drop. Remember that the most common reason for a 40 point drop is due to balance changes. … An old credit card account closed.