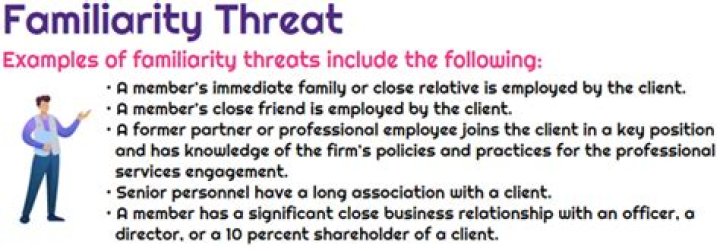

What does familiarity threat mean

A familiarity threat is the threat that due to a long or close relationship with a client or employer, a professional accountant will be too sympathetic to their interests or too accepting of their work (100.12(d)).

Which of the following is not an example of a familiarity threat?

d. Occurs when a firm, or a member of the assurance team, promotes, or may be perceived to promote, an assurance client’s position or opinion to the point that objectivity may, or may be perceived to be, compromised. 59.

What is a intimidation threat?

From Wikipedia, the free encyclopedia. Intimidation (also called cowing) is intentional behavior that would cause a person of reasonable apprehension to fear injury or harm. It is not necessary to prove that the behavior caused the victim to experience terror or panic.

What is a self interest threat?

Section 200.8 A6 describes self-interest threat as: “The threat that a member could benefit, financially or otherwise, from an interest in, or relationship with, the employing organisation or persons associated with the employing organisation.How do you get rid of familiarity threats?

- Changing the role of the senior personnel on the attest engagement team or the nature and extent of the tasks the senior personnel perform.

- Having a professional accountant who was not included on the attest engagement team review the work of the senior personnel.

What is an example of familiarity threat?

A familiarity threat exists if the auditor is too personally close to or familiar with employees, officers, or directors of the client company. ABC Company has been audited by the same auditor for over 10 years and the auditor regularly plays golf with the CEO and CFO of ABC Company.

How do you mitigate a familiarity threat?

The familiarity threat to the independence of the auditor is when auditors let their familiarity with the client influence their decisions. This threat may stem from experiences or relationships with the client. In most cases, auditors can avoid the familiarity threat by removing the affected auditor from the team.

What are ethical threats?

An ethical threat is a situation where a person or corporation is tempted not to follow their code of ethics. An ethical safeguard provides guidance or a course of action which attempts to remove the ethical threat.What does professional skepticism mean?

Professional skepticism is an attitude that includes a questioning mind and a critical assessment of audit evidence. … In exercising professional skepticism, the auditor should not be satisfied with less than persuasive evidence because of a belief that management is honest.

What are the five codes of ethics?- Integrity.

- Objectivity.

- Professional competence.

- Confidentiality.

- Professional behavior.

How do you avoid self-review threats?

The most effective safeguard against the self-review threat is the segregation of teams. Audit firms that provide non-audit services to clients must use separate members for each assignment. This way, they will never face the threat of having to review their own work.

Which of the following is an example of self interest threat?

Self interest threat Examples include: When the auditor or a member of their family owns shares in a client. They would directly benefit from increases in client profits and would be reluctant to raise any concerns that could adversely affect the performance of the client.

What is considered a verbal threat?

A verbal threat is a statement made to someone else in which the speaker declares that they intend to cause the listener harm, loss, or punishment. Although this definition sounds very similar to the definition for assault, simply uttering threatening words to another person will most likely not count as an assault.

What is considered threatening behavior?

Threatening behavior means acts which would cause a reasonable person to fear unlawful sexual conduct, unlawful restraint, bodily injury, or death, including verbal threats,; written, telephonic, or other electronically communicated threats,; vandalism,; or physical contact without consent.

Can u go to jail for threatening someone?

Whoever commits the offence of criminal intimidation shall be punished with imprisonment of either description for a term which may extend to two years, or with fine, or with both; If threat be to cause death or grievous hurt, etc.

What are the two main categories of safeguards against threats to our fundamental ethical principles that can be put in place?

Ethical safeguards can be grouped into two broad categories: i. Safeguards created externally, by legislation, regulation or the accountancy profession ii. Safeguards established within the work environment.

Is audit a risk?

Audit risk is a function of the risks of material misstatement and detection risk‘. Hence, audit risk is made up of two components – risks of material misstatement and detection risk.

How do you ensure auditor independence?

The SEC rules on audit independence are often organized into five key areas: (A) Prohibited Non-Audit Services; (B) Audit Committee Pre-Approval of Services; (C) Partner Rotation; (D) Conflict of Interest; and (E) Increased Communication and Disclosure.

What impairs auditor independence?

Independence will be considered to be impaired if, during the period of a professional engagement, a member or his or her firm had any cooperative arrangement with the client that was material to the member’s firm or to the client.

What makes an auditor independent?

Independence requires integrity and an objective approach to the audit process. The concept requires the auditor to carry out his or her work freely and in an objective manner. Independence of the internal auditor means independence from parties whose interests might be harmed by the results of an audit.

Can an auditor ever be truly independent?

Ultimately, as long as audit appointments and fees are determined by the company being audited, the auditor can never truly be economically independent of the client. That is why there are broader codes of conduct which govern the relationship between both parties.

What is the period of professional engagement?

289 Period of the professional engagement. The period of the professional engagement begins when a member either signs an initial engagement letter or other agreement to perform attest services or begins to perform an attest engagement for a client, whichever is earlier.

What is safeguard in audit?

Safeguards are actions or other measures that may are appropriate to eliminate threats or. reduce them to an acceptable level. • Safeguards are actions or other measures that may will reasonably eliminate threats or reduce. them to an acceptable level.

What are two common judgment traps?

Prawitt identified confirmation bias and a phenomenon the white paper calls judgment “triggers” as two particularly damaging “traps” that lead to poor judgment and decisions.

What is Operation Broken gate?

Internally designated “Operation Broken Gate,” the Enforcement Division’s efforts seek to identify auditors who fail to carry out their duties and responsibilities consistent with professional standards.

How can professional Scepticism be improved?

Application of Good Judgment Process: An important way to improve professional skepticism in individual auditors is to accelerate their ability to exercise sound judgment by following a good judgment process and learning to avoid judgment traps and biases.

What are the 7 principles of ethics?

- beneficence. good health and welfare of the patient. …

- nonmaleficence. Intetionally action that cause harm.

- autonomy and confidentiality. Autonomy(freedon to decide right to refuse)confidentiality(private information)

- social justice. …

- Procedural justice. …

- veracity. …

- fidelity.

What are 5 fundamental principles?

Research the meaning of the five fundamental political principles: consent of the governed, limited government, rule of law, democracy, and representative government.

What are the 3 requirements of ethics?

- Respect for Persons. …

- Beneficence. …

- Justice.

What are threats in auditing?

When auditors want to take up a new engagement or continue an existing one, they must ensure their independence and objectivity. However, there are several threats that may threaten them. These include self-interest, self-review, familiarity, intimidation, and advocacy threats.

Can a CPA auditor be independent without being objective?

It is possible for someone to be independent but not objective, and it is equally possible for someone to be objective without being independent. … Standard 1100 states: “The internal audit activity must be independent and internal auditors must be objective in performing their work.”