What is a Desktop Underwriter

Desktop Underwriter (DU) is an automated underwriting system developed by Fannie Mae to help mortgage lenders make informed credit decisions on conventional and government loans. … It then covers how to interpret underwriting recommendations and review reports accurately.

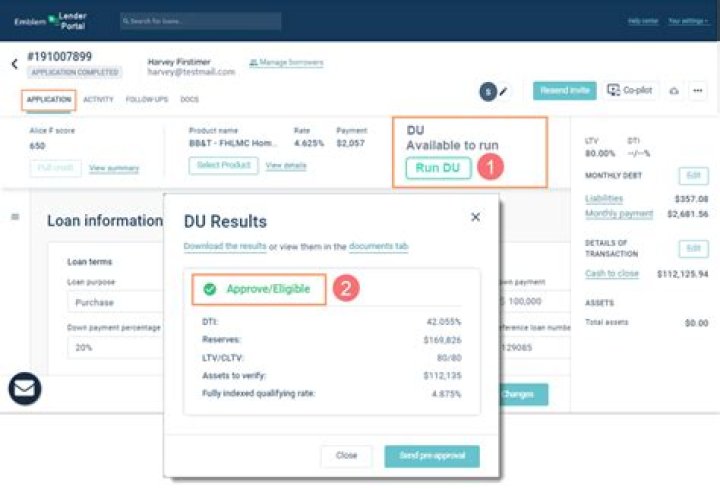

What is a Desktop Underwriter approval?

Desktop Underwriter is an automated system for mortgage underwriting that calculates if a loan meets approval requirements. It is used by Fannie Mae and, in some cases, the Federal Housing Authority. The program uses Form 1003 plus more than 75 third-party vendors to predict if the borrower will be approved for a loan.

How do I add sponsoring lender to desktop originator?

- Select Sponsor. …

- Select the institution(s) that you want the originator to use for submitting loan application data, and then click Continue.

- On the confirmation screen, click Continue to confirm that you want to sponsor the originator.

Is Desktop Underwriter free?

Fannie Mae currently offers Collateral Underwriter and EarlyCheck to lenders at no charge to encourage lender use and drive industry-wide collateral and data quality. Effective immediately, Fannie Mae will offer Desktop Underwriter and Desktop Originator on a no-fee basis, as well.What is FNMA and Fhlmc?

These are Government backed subsidized loans. The meaning is FNMA = Fannie Mae and FHLMC = Freddie Mac. … We can help you apply with either agency, depending on your individual loan criteria.

Can you be denied in underwriting?

Even if you are pre-approved, your underwriting can still be denied. … Your loan is never fully approved until the underwriter confirms that you are able to pay back the loan. Underwriters can deny your loan application for several reasons, from minor to major.

What is DU and LP in mortgage?

DU stands for Desktop Underwriter and LP stands for Loan Prospector. … Loan originators use DU and LP to determine whether a loan meets Fannie Mae or Freddie Mac’s eligibility requirements which means DU or LP approval is a critical step towards closing on a mortgage.

What FICO score is typically used to qualify a borrower?

The commonly used FICO® Scores for mortgage lending are: FICO® Score 2, or Experian/Fair Isaac Risk Model v2. FICO® Score 5, or Equifax Beacon 5. FICO® Score 4, or TransUnion FICO® Risk Score 04.What does underwriter look for?

An underwriter is a financial expert who takes a look at your finances and assesses how much risk a lender will take on if they decide to give you a loan. More specifically, underwriters evaluate your credit history, assets, the size of the loan you request and how well they anticipate that you can pay back your loan.

Is LP Fannie or Freddie?Fannie Mae uses the automated underwriting system called Desktop Underwriter or DU, while Freddie Mac uses the AUS called Loan Prospector or LP.

Article first time published onWhat is a DU letter?

The Pre-approval letter is written by a Loan Officer and is submitted by the Buyer along with their Purchase Agreement. … There is also a program called Desktop Underwriting, or DU which allows Loan Officers to run the Buyers’ scores and data through an automated underwriting program to be sure of their qualifications.

Is AmeriSave Fannie Mae?

AmeriSave offers a full range of loan types and terms to suit every home buyer. Loan types include fixed rate, adjustable rate, FHA, VA, USDA mortgages and more. AmeriSave is a direct seller to Fannie Mae, Freddie Mac and Ginnie Mae.

What is Freddie Mac LPA?

Loan Product Advisor is our enhanced automated underwriting system. It helps simplify your origination processes and provides you with greater certainty that your loans meet Freddie Mac eligibility requirements.

What is a sponsoring lender?

Sponsoring Lender means any third-party financial institution (i) which selects Licensee to offer its mortgage loan products and to communicate with such institution by means of the Licensed Application, which communication includes the submission and receipt of mortgage loan product information and Licensee’s …

What is difference between conforming and nonconforming loan?

A conforming loan meets the guidelines to be sold to either Fannie Mae or Freddie Mac, two of the largest mortgage buyers in the U.S. Non-conforming loans, on the other hand, are those that fall outside those guidelines, so they can’t be sold to Fannie Mae or Freddie Mac.

When was Fhlmc created?

As we mentioned earlier, Freddie Mac is not an actual person but is instead a variant of the initials of the company’s full name, the Federal Home Loan Mortgage Corporation or FHLMC. Freddie Mac was created in 1970 as part of the Emergency Home Finance Act to expand the secondary mortgage market in the United States.

Why is it called Fannie Mae?

So, to break down the acronyms: Fannie Mae, or the Federal National Mortgage Association, came from the acronym FNMA. Fannie for the letters “FN” and Mae for “MA.” Ginnie Mae, or Government National Mortgage Association, came from its acronym GNMA.

What is LP mortgage?

LP, which stands for Loan Prospector, is the Freddie Mac automated underwriting service used by third-party loan originators and mortgage wholesale lenders that provides risk assessment for Freddie Mac’s credit and pricing terms.

What is the difference between Freddie and Fannie?

The primary difference between Freddie Mac and Fannie Mae is where they source their mortgages from. Fannie Mae buys mortgages from larger, commercial banks, while Freddie Mac buys them from much smaller banks.

What is an Aus approval?

The automated underwriting system approval is what is needed to proceed with the mortgage approval process. … The automated underwriting system is the use and utilization of computers to underwrite mortgage loans. The automated underwriting system approval, also known as AUS, has made mortgage approvals automated.

Is no news good news with underwriting?

When it comes to mortgage lending, no news isn’t necessarily good news. … Particularly in today’s economic climate, many lenders are struggling to meet closing deadlines, but don’t readily offer up that information.

Do underwriters want to approve loans?

An underwriter will approve or reject your mortgage loan application based on your credit history, employment history, assets, debts and other factors. It’s all about whether that underwriter feels you can repay the loan that you want. … But a seasoned loan originator is the integral part of the whole process, he says.

What can go wrong during underwriting?

The main thing that could go wrong in underwriting has to do with the home appraisal that the lender ordered: Either the assessment of value resulted in a low appraisal or the underwriter called for a review by another appraiser. … You can contest a low appraisal, but most of the time the appraiser wins.

How often do underwriters deny loans?

One in every 10 applications to buy a new house — and a quarter of refinancing applications — get denied, according to 2018 data from the Consumer Financial Protection Bureau.

Can my loan be denied at closing?

Can a mortgage loan be denied after closing? Though it’s rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. “It’s not unheard of that before the funds are transferred, it could fall apart,” Rueth said.

How do I know if my mortgage will be approved?

- Your credit score. Your credit score is determined based on your past payment history and borrowing behavior. …

- Your debt-to-income ratio. …

- Your down payment. …

- Your work history. …

- The value and condition of the home.

How far back do Mortgage Lenders look at credit history?

The typical timeframe is the last six years. There are many factors that lenders consider when looking at your credit history, and each one is different. The typical timeframe is the last six years, but there are many different factors that lenders look at when reviewing your mortgage application.

What credit score is needed to buy a house 2020?

Generally speaking, you’ll need a credit score of at least 620 in order to secure a loan to buy a house. That’s the minimum credit score requirement most lenders have for a conventional loan.

What is the most important credit score?

- Payment History – this is the most important and accounts for 35% of your FICO 8 Score. …

- Credit Usage – the amount of credit you are using accounts for 30% of your credit score. …

- Length of Credit History – A long credit history accounts for 15% of your Score.

What AUS does FHA use?

The FHA Catalyst: Single Family Origination Module–AUS is an automated underwriting option for lenders to use, but will not be required to replace lender use of other automated underwriting systems that accommodate FHA-insured mortgages through interfaces with FHA’s TOTAL Mortgage Scorecard.

Is Freddie Mac more lenient than Fannie Mae?

Pros And Cons On Fannie Mae Versus Freddie Mac Freddie Mac is more lenient with mortgage loan applicants with poor credit history and lower credit scores. Freddie Mac is also laxer on higher debt to income ratios. This is so especially those mortgage loan applicants with debt to income ratios as high as 50% DTI.