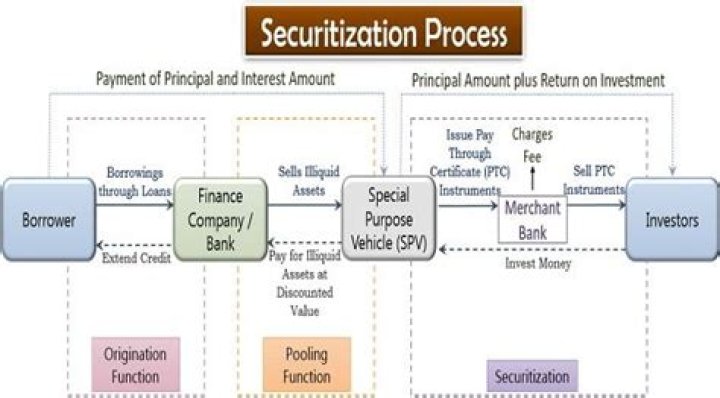

What is a loan securitization

Unlike the more traditional relationship between a borrower and a lender, securitization involves the sale of the loan by the lender to a new owner–the issuer–who then sells securities to investors. The investors are buying ‘bonds’ that entitle them to a share of the cash paid by the borrowers on their mortgages.

Can auto loan be securitized?

The securitization of auto loans is actually the securitization of retail installment sales contracts that are backed by autos and light trucks. The maximum maturity of the loan is 60 months and the loans pay principal and interest on a monthly basis.

What is the concept of securitization?

Securitization is the procedure where an issuer designs a marketable financial instrument by merging or pooling various financial assets into one group. … In theory, any financial asset can be securitized—that is, turned into a tradeable, fungible item of monetary value.

What is an example of securitization?

Securitization is the process of taking an illiquid asset or group of assets and, through financial engineering, transforming it (or them) into a security. … A typical example of securitization is a mortgage-backed security (MBS), a type of asset-backed security that is secured by a collection of mortgages.Why do companies go for securitization?

Securitization converts loan relationships into capital market commodities and therefore, increases the power of the capital market. Debate on the potential risks of the capital market-financial market connectivity was initiated (or carried forward) by Prof Henry Kaufman.

Why do banks securitize loans?

Banks may securitize debt for several reasons including risk management, balance sheet issues, greater leverage of capital, and in order to profit from origination fees. … The bank then sells this group of repackaged assets to investors.

How do I know if my loan was securitized?

If one of the federal agencies bought your mortgage, then it’s a sure bet it’s been securitized. If it’s owned by some other company, you can contact it and ask to know whether your mortgage has been securitized.

What are the assets suitable for securitization?

Here are a few examples of assets that can be securitized: Residential mortgage loans; this category includesthe infamous “subprime mortgages,” which are home loans issued to individualswith a low credit rating. Commercial mortgage loans. Bank loans to businesses.How does debt securitization work?

The Process of Securitization Depending on the situation, the SPV issues the bonds directly or pays the originator the balance on the debt that is sold, which increases the liquidity of the assets. The debt is then divided into bonds, which are sold on the open market.

What are the risks of securitisation?Bad debts arise when borrowers default on their loans. This is one of the primary risks associated with securitized assets, such as mortgage-backed securities (MBS), as bad debts can stop these instruments’ cash flows. The risk of bad debt, however, can be apportioned among investors.

Article first time published onIs securitisation good or bad?

Securitization is an exceptionally clever process that has very significant benefits for practically everyone involved. It takes debt off a balance sheet and replaces it with liquidity. It provides third-party investors with clearly rated investments that pay according to the risk that they are willing to shoulder.

Are all mortgages securitized?

Most mortgages are securitized, meaning the loans are sold and pooled together to create a mortgage security that is traded in the capital markets for profit. Though these securitizations can take many different forms, they are generally referred to as mortgage-backed securities, or MBS.

How did securitization cause the financial crisis?

Securitization is now regarded as one of the main causes of the 2007-2009 financial crisis. Securitization active banks displayed opportunistic behaviour by lowering lending standards and selling lower quality collateralised assets to unsuspecting third parties.

Who invented securitization?

Lew Ranieri. Meet the father of mortgage-backed bonds. In the late 1970s, the college dropout and Salomon trader coined the term securitization to name a tidy bit of financial alchemy in which home loans were packaged together by Wall Street firms and sold to institutional investors.

Who is originator in securitisation?

The Originator is the entity that assigns assets or risks in a securitisation transaction. Usually it is the party (lender) who originally underwrote and securitised the claims (loans).

What advantages does securitization offer to the lending institutions?

The benefit to financial institutions is that securitization frees up regulatory capital — the assets that banks are required to hold by their financial regulators to remain solvent. In addition, securitization can offer issuers higher credit ratings and lower borrowing costs.

What is securitization and why is it used?

securitization represents an alternative and diversified source of finance based on the transfer of credit risk (and possibly also interest rate and currency risk) from issuers to investors. … Securitization was initially used to finance simple, self- liquidating assets such as mortgages.

What percentage of mortgages are securitized?

In part for this reason, an increasing share of home mortgages have been securitized, with the ratio of MBSs to total mortgages now over 50% (see figure 2).

Why did banks believe that mortgage-backed securities?

Why did banks believe that mortgage-backed securities protected them from defaults? Multiple choice question. Home values were expected to continually rise. Loans within mortgage-backed securities had very low interest rates.

What is meant by systemic risk?

Systemic risk refers to the risk of a breakdown of an entire system rather than simply the failure of individual parts. In a financial context, if denotes the risk of a cascading failure in the financial sector, caused by linkages within the financial system, resulting in a severe economic downturn.

Why did mortgage-backed securities fail?

Hedge funds, banks, and insurance companies caused the subprime mortgage crisis. Hedge funds and banks created mortgage-backed securities. … When the Federal Reserve raised the federal funds rate, it sent adjustable mortgage interest rates skyrocketing. As a result, home prices plummeted, and borrowers defaulted.