What is the 6 month repricing gap

So, for example, to calculate the 6-month gap, one must take into account all fixed-rate assets and liabilities that mature in the next 6 months, as well as the variable-rate assets and liabilities to be repriced in the next 6 months. The gap, then, is a quantity expressed in monetary terms.

What is repricing gap analysis?

The repricing gap is a measure of the difference between the dollar value of assets that will reprice and the dollar value of liabilities that will reprice within a specific time period, where reprice means the potential to receive a new interest rate.

What is the one year repricing gap?

Repricing Gap is the difference between the repriced assets and the repriced liabilities. The assets and liabilities are repriced on the basis of changed interest rates. These are repriced for a specific time horizon like 6 moths, one year, five years etc.

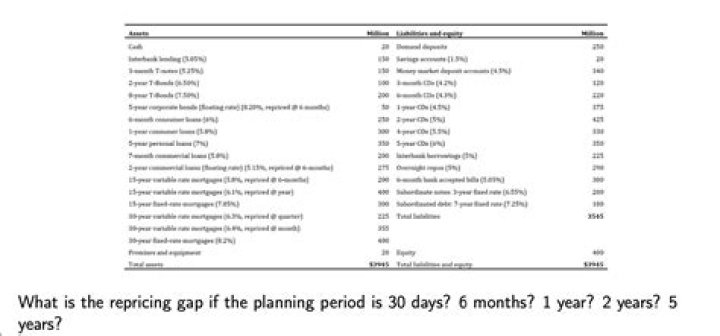

What is the repricing gap if the planning period is 30 days?

Funding or repricing gap using a 30-day planning period = 75 – 170 = -$95 million. Funding gap using a 91-day planning period = (75 + 75) – 170 = -$20 million. Q2. Net interest income will decline by $475,000.How is Bank gap calculated?

Formula and Calculation of the Interest Rate Gap The interest rate gap is calculated as interest rate sensitive assets minus interest rate sensitive liabilities.

What is RSA and RSL?

• RSA = all the assets that mature or are repriced within the. gapping period (maturity bucket) • RSL = all the liabilities that mature or are repriced within. the gapping period (maturity bucket)

How do you calculate maturity gap?

Longer repricing periods have a higher sensitivity to interest rate changes and are subject to any change over the intervening year. An asset or a liability with an interest rate that cannot change for more than a year is considered fixed.

What is the formula for net interest margin?

Net Interest Margin Using Formula is calculated as: Net Interest Margin = (Net return on investment – Interest paid) / Average Assets. Net Interest Margin = (25,000 – 9,000) /100,000.How do you calculate risk of refinance?

The firms’ refinancing risk is measured by the maturing portion of outstanding long-term debt. The result shows that firms with a high refinancing risk choose longer maturities. This effect is stronger for speculative-grade and low-cash-flow firms.

What is WatchoverU's expected net interest income at year end?What is WatchoverU’s expected net interest income at year-end? Current expected interest income: $50m(0.10) + $50m(0.07) = $8.5m. Expected interest expense: $70m(0.06) – $20m(0.07) = $5.6m.

Article first time published onIs it reasonable for changes in interest rates on RSAs and RSLs to differ Why?

It is not uncommon for interest rates to adjust in an unequal manner on RSAs versus RSLs. Interest rates often do not adjust solely because of market pressures. In many cases the changes are affected by decisions of management. Thus, you can see the difference between this answer and the answer for part a.

What is desired repricing period?

Repricing period, also referred to as cycle, tenor, or fixing period, is the period for which the interest indicated will apply. After this period interest rates will be repriced, to either go up or down depending on economic factors prevailing at the time of repricing.

What is next repricing date?

Reprice Date means the first day of each month.

What is repricing bucket?

The first tool used by e-Bank to control its interest rate exposure on the banking book is the repricing bucket (also called ‘repricing gap’ or ‘interest rate sensitivity’ table). The repricing bucket provides information about the time of repricing of all assets and liabilities.

How is liquidity gap calculated?

A liquidity gap is calculated as assets minus liabilities. For a company, this would be all assets, such as cash and marketable securities, and all liabilities, such as short-term debt.

What is a gap ratio?

Gap ratio is the ratio of a company’s rate sensitive assets to liabilities. ‘Rate sensitive’ means that the assets and liabilities rise or fall significantly when interest rates change. In other words, gap ratio is the measurement of a business’ short-term investments against short-term expenditure.

Why is it useful to express the repricing gap as a gap ratio?

Runoff in demand deposits in a repricing model is typically lower during periods of falling interest rates. The gap ratio is useful because it indicates the scale of the interest rate exposure by dividing the gap by the asset size of the institution.

What is gap analysis investopedia?

A gap analysis is the process companies use to compare their current performance with their desired, expected performance. … A gap analysis is the means by which a company can recognize its current state—by measuring time, money, and labor—and compare it to its target state.

What does repricing mean?

Repricing occurs when a company retires employee stock options that have become quite out-of-the-money with new options that have a lower strike price. … By repricing, the company effectively replaces now-worthless options with those that have value in order to keep top managers or key employees.

What is meant by Tier 1 capital?

Tier 1 capital consists of shareholders’ equity and retained earnings—disclosed on their financial statements—and is a primary indicator to measure a bank’s financial health. … Tier 1 capital is the primary funding source of the bank. Typically, it holds nearly all of the bank’s accumulated funds.

What is ALM report?

ALM Reporting provides you with the must-have components of a trusted asset/liability management report: Economic Value Analyses (NEV / EVE) Net Interest Income Simulations (NII) Non-Maturity Deposit Analysis.

Are federal funds rate sensitive assets?

Domestically, most other lending rates are derived either from the Prime Rate, the Fed Funds Rate, or from the London Inter-bank Offered Rate (LIBOR),. Interest-sensitive assets are the financial products that are most affected by changes in borrowing rates.

What is equity market risk?

Equity risk is the risk involved in the changing prices of stock investments, and commodity risk covers the changing prices of commodities such as crude oil and corn. Currency risk, or exchange-rate risk, arises from the change in the price of one currency in relation to another.

What is interest rate refinancing risk?

Refinancing risk, in banking and finance, is the possibility that a borrower cannot refinance by borrowing to repay existing debt. … Refinancing risk increases during rising interest rates, as the borrower may not have sufficient income to afford the higher interest rate on a new loan.

What is refinancing risk explain with example?

Refinancing Risk refers to the risk arising out of the inability of the individual or an organization to refinance its existing debt due to redemption with new debt. Refinancing risk carries the risk of the failure of the business to roll over its debt obligation and, as such, also known as rollover risk.

What is a good NIM?

NIM is one indicator of a bank’s profitability and growth. The average NIM for U.S. banks was 3.3% in 2018. The long-term trend has been downward since 1996 when the average was 4.3%.

What is the difference between NII and NIM?

What Is NII and NIM? NII or net interest income is the difference between the income a bank earns from its lending activities and the interest it pays to depositors whereas NIM or net interest margin is calculated by dividing NII by the average income earned from interest-producing assets.

How can I improve my NIM?

- Focus on liquidity. …

- Monitor cash and cash equivalents. …

- Focus on three numbers: Total loans, total deposits and loans-to-deposits ratio. …

- Think long-term on deposit rates. …

- Look for opportunities to invest idle funds. …

- Create open communication and transparency.

What is a maturity bucket in the repricing gap model Why is the length of time selected for repricing assets and liabilities important when using the repricing gap model?

Why is the length of time selected for repricing assets and liabilities important when using the repricing model? The maturity bucket is the time window over which the dollar amounts of assets and liabilities are measured.

When CGAP is positive an equal increase in interest rates for RSAs and RSLs will result in an increase in net interest income?

In general, when CGAP is positive, the change in NII is positively related to the change in interest rates. Conversely, when CGAP (or the gap ratio) is negative, if interest rates rise by equal amounts for RSAs and RSLs (row 3, Table 8–3 ), NII will fall (since the FI has more RSLs than RSAs).

What is a negative gap?

A negative gap is a situation where a financial institution’s interest-sensitive liabilities exceed its interest-sensitive assets. A negative gap is not necessarily a bad thing, because if interest rates decline, the entity’s liabilities are repriced at lower interest rates. In this scenario, income would increase.