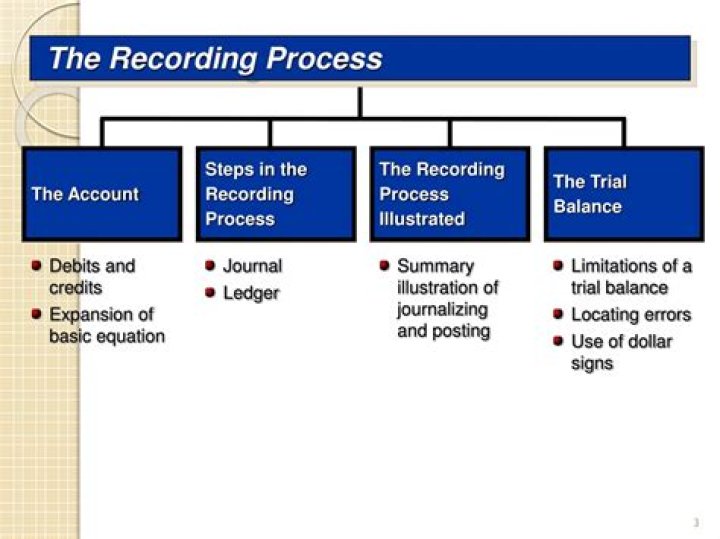

What is the recording process

The basic steps in the recording process are (1) analyze each transaction for its effects on the accounts, (2) enter the transaction information in a journal, and (3) transfer the journal information to the appropriate accounts in the ledger.

What are the steps in the recording process in accounting?

- Step 1: Identify Transactions. …

- Step 2: Record Transactions in a Journal. …

- Step 3: Posting. …

- Step 4: Unadjusted Trial Balance. …

- Step 5: Worksheet. …

- Step 6: Adjusting Journal Entries. …

- Step 7: Financial Statements. …

- Step 8: Closing the Books.

What is the purpose of the recording process?

The process recording helps the student conceptualize and organize ongoing activities with client systems, to clarify the purpose of the interview or intervention, to improve written expression, to identify strengths and weaknesses, and to improve self- awareness (Urbanowski & Dwyer, 1988).

What is recording system in accounting?

Learn About the 8 Important Steps in the Accounting Cycle Accounting.What is recording in accounting class 11?

Recording of Transactions 1 is considered as a process of executing accounting transactions of a business in different books of accounts. Recording of Transactions Class 11 makes use of cash book, journal book, a ledger account, profit & loss a/c, etc.

What are the 7 steps of accounting cycle?

We will examine the steps involved in the accounting cycle, which are: (1) identifying transactions, (2) recording transactions, (3) posting journal entries to the general ledger, (4) creating an unadjusted trial balance, (5) preparing adjusting entries, (6) creating an adjusted trial balance, (7) preparing financial …

What is the difference between GL and TB?

Comparing the General Ledger and Trial Balance The general ledger contains the detailed transactions comprising all accounts, while the trial balance only contains the ending balance in each of those accounts.

Where are transactions recorded?

Consideration must be taken when numbers are inputted into the debit and credit sections. Then, finally, the transaction is recorded in a document called a journal. A journal is the first place that a transaction is written in accounting records.Which is not part of the recording process?

The correct option is (b) Preparing a trial balance. Trial balance is not used for recording the transactions of the business.

Why is recording accounting important?You need good records to prepare accurate financial statements. These include income (profit and loss) statements and balance sheets. These statements can help you in dealing with your bank or creditors and help you manage your business.

Article first time published onWhat is the process of recording business transactions?

Recording business transactions is a multi-step process. The first step in recording business transactions is to examine the transaction and decide what accounts will be affected. The second step in recording business transactions is to decide what account will be debited and what account will be credited.

How do you record bookkeeping?

- Create a New Business Account.

- Set Budget Aside for Tax Purposes.

- Always Keep Your Records Organised.

- Track Your Expenses.

- Maintain Daily Records.

- Leave an Audit Trail.

- Stay on Top of Your Accounts Receivable.

- Keep Tax Deadlines in Mind.

Why are financial transactions recorded in accounting?

Dear Student, Only Financial Transactions are to be recorded in accountancy because it is due to Money Measurement Concept , which states that only those transactions are to be recorded in books of accounts which are measurable in terms of money. Hence , it is concerned with the Nominal value not the real value .

What is used in single entry bookkeeping as basic records?

The single-entry method is the foundation of cash-basis accounting. With the single-entry system of bookkeeping, you mostly record cash disbursements and cash receipts. You will record incoming and outgoing money in the cash book. Usually, you track assets and liabilities separately.

What is theory base of accounting?

The theory base of accounting consists of principles, concepts, rules and guidelines developed over a period of time to bring uniformity and consistency to the process of accounting and enhance its utility to different users of accounting information.

Who prepares trial balance?

A company prepares a trial balance periodically, usually at the end of every reporting period. The general purpose of producing a trial balance is to ensure the entries in a company’s bookkeeping system are mathematically correct.

What is Journal and trial balance?

At the end of an accounting period, after all the journal entries are made and posted, a trial balance is generated. The trial balance is a listing of all the accounts that a business has and their balances.

What is the relation between journal and ledger?

Journal is a subsidiary book of account that records transactions. Ledger is a principal book of account that classifies transactions recorded in a journal. The journal transactions get recorded in chronological order on the day of their occurrence.

What are the records used in accounting cycle?

The key steps in the eight-step accounting cycle include recording journal entries, posting to the general ledger, calculating trial balances, making adjusting entries, and creating financial statements.

What are the 4 phases of accounting and explain each?

There are four basic phases of accounting: recording, classifying, summarizing and interpreting financial data. Communication may not be formally considered one of the accounting phases, but it is a crucial step as well.

What are the 5 major transaction cycles?

- Revenue cycle—Interactions with customers. …

- Expenditure cycle—Interactions with suppliers. …

- Production cycle—Give labor and raw materials; get finished product.

- Human resources/payroll cycle—Give cash; get labor.

- Financing cycle—Give cash; get cash.

How often does the recording process occur?

Recording process should occur repeatedly during the accounting period in order to represent the information on periodic…

How many accounts are there in a ledger?

General ledger representing the five main account types: assets, liabilities, income, expenses, and capital.

What does T account mean?

A T-account is an informal term for a set of financial records that uses double-entry bookkeeping. … The title of the account is then entered just above the top horizontal line, while underneath debits are listed on the left and credits are recorded on the right, separated by the vertical line of the letter T.

How do you record following transactions?

- Personal account rule. Debit- The receiver. Credit- The giver.

- Real account rule. Debit- What comes in. Credit- What goes out.

- Nominal account rule. Debit- All expenses and losses. Credit- All incomes and gains.

- Now. The journal entries will be. Sales Return A/C DR ₹ 2,000. To Mahaveer’s A/C ₹ 2,000.

Where do we first record a transaction?

A transaction should be recorded first in a journal because journal provides complete details of a transaction in one entry. Further, a journal forms the basis for posting the transactions into their respective accounts into ledger.

How do you record transactions in general ledger?

- Create journal entries.

- Make sure debits and credits are equal in your journal entries.

- Move each journal entry to its individual account in the ledger (e.g., Checking account)

- Use the same debits and credits and do not change any information.

What are the advantages of recording transactions?

Recording transactions allows you to prepare finances for tax returns, therefore meeting deadlines and avoiding penalties. Your tax returns should always be completed across the year and well in advance of any deadlines, ensuring any minor errors can be altered before it becomes a big problem.

How do you record transactions in accounting equation?

Transaction TypeAssetsLiabilities + EquityPay dividendsCash decreasesRetained earnings (equity) decreases

What is the process of recording a transaction in the journal called?

The process of recording transaction into journal is called Journalising.

How do you record finances?

- Check your account statements. …

- Categorize your expenses. …

- Use a budgeting or expense-tracking app. …

- Explore other expense trackers. …

- Identify room for change.