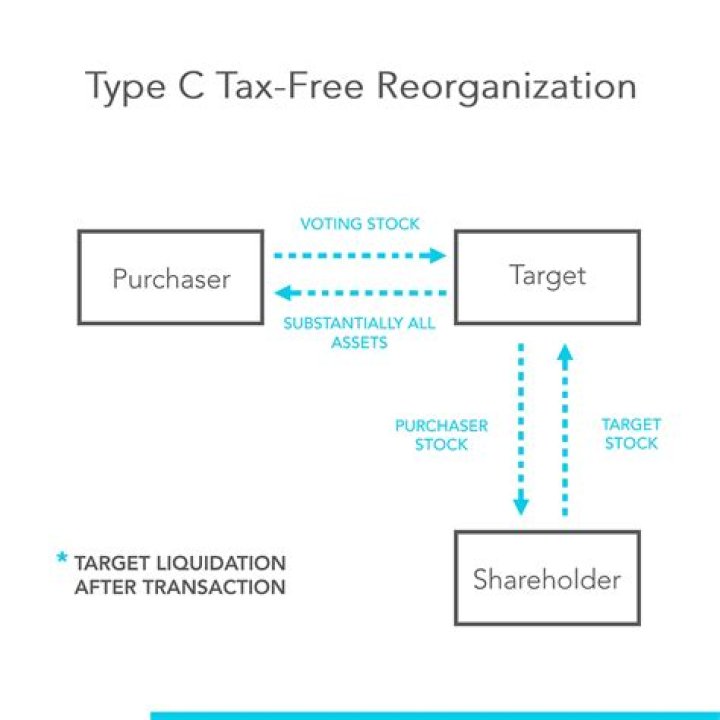

What is Type C reorganization

A C-reorganization, otherwise known as a “practical merger,” is where a target. corporation (“Target”) transfers “substantially all” of its properties to an acquiring. corporation (“Acquiror”) solely in exchange for all or a part of Acquiror’s “voting.

What is a triangular B reorganization?

A triangular B reorganization is an acquisition by S of T stock in exchange for P stock in a transaction that qualifies as a reorganization under section 368(a)(1)(B).

What is a Type A acquisition?

A Type “A” acquisition has the following characteristics: At least 50% of the payment must be in the stock of the acquirer. The selling entity is liquidated. The acquirer acquires all assets and liabilities of the seller.

What determines if an acquisition is taxable or tax-free?

The buyer must acquire “substantially all” of the target’s assets (defined as at least 70% and 90% of the FV of the target’s gross assets and net assets, respectively) for the transaction to qualify for tax-free treatment.What is F reorganization?

The I.R.C. defines a F Reorganization as “a mere change in identity, form, or place of organization of one corporation, however effected.”[1] This mere change can be accomplished in many ways and for different reasons.

What is a section 368 Reorganization?

Internal Revenue Code (IRC) Section 368 allows merger and acquisition transactions to qualify as a reorganization when an acquiring corporation gives a substantial amount of its own stock as consideration to the acquired (or “target”) corporation.

What is a cash D reorganization?

368(a) (1)(D) (a D reorganization) generally involves a transfer by one corporation (target corporation) of all or a part of its assets to another corporation (acquiring corporation) if, immediately after the transfer, the target corporation or one or more of its shareholders, or any combination thereof, is in control …

Why do a reverse triangular merger?

One of the reasons to pursue reverse cash or triangular merger is the ability to maintain the target company’s legal status, which helps it preserve contracts and other nontransferable assets. Also, the transaction structure makes it easier to squeeze out minority shareholders or cash out options.What is a tax free reorganization?

Certain types of corporate acquisitions, divisions, and other restructurings which are generally not taxable at the corporate or stockholder level. The transaction must meet strict statutory and non-statutory requirements (see IRC § 368 and Treasury Regulations ).

Does tax matters on acquisition?At the corporate level, the tax treatment of a merger or acquisition depends on whether the acquiring firm elects to treat the acquired firm as being absorbed into the parent with its tax attributes intact, or first being liquidated and then re- ceived in the form of its component assets.

Article first time published onHow are acquisitions taxed?

Broadly speaking, acquisitions can be structured as either asset or stock sales. In a taxable stock acquisition, the buyer acquires stock from the target company’s shareholders, who are taxed on the difference between the purchase price and their outside basis in the target’s stock.

What happens to deferred tax assets in an acquisition?

A deferred tax asset would be recorded in acquisition accounting because the liability, when settled, will result in a future tax deduction. That is, a deferred tax asset is recognized at the acquisition date since there is a basis difference between book and tax related to the liability.

What are the four types of acquisitions?

- Horizontal Acquisition. This is when a company acquires another company in the same business, or industry or sector, that is, a competitor. …

- Vertical Acquisition. …

- Conglomerate Acquisition. …

- Congeneric Acquisition.

What are the two types of acquisitions?

- Stock purchase. In a stock purchase, the buyer acquires the stock of the target company from its stockholders. …

- Asset purchase. In an asset purchase, the buyer only buys the assets and liabilities that are precisely specified in the purchase agreement. …

- Merger.

What are the different types of acquisitions?

- Vertical Acquisition.

- Horizontal Acquisition.

- Conglomerate Acquisition.

- Market Extension Acquisitions.

- Know Your Mergers.

Is an S corporation?

S corporations are corporations that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. … S corporations are responsible for tax on certain built-in gains and passive income at the entity level.

Can a C Corp do an F reorg?

While F reorganizations can also be used with C corporations, an F reorganization is particularly well suited for a variety of transactions involving S corporations. All section references herein, other than to Regulations, are to the Internal Revenue Code of 1986, as amended. Reg. § 1.368-2(m)(1).

What is a qualified S Corp subsidiary?

A qualified subchapter S subsidiary (QSub) is a subsidiary corporation 100% owned by an S corporation that has made a valid QSub election for the subsidiary (Sec. … The QSub election terminates the QSub’s former identity as a separate entity for federal tax purposes. Thus, a final income tax return must be filed.

Does section 368 apply to S corps?

Therefore, the tax-free reorganization rules in IRC Section 368 apply to both C- and S-corporations. In a tax-free reorganization, an S-corporation can be the target corporation or acquiring corporation, or both. … It is also possible for both parties to a tax-free reorganization to be S-corporations.

What is an upstream C reorganization?

An upstream C with a drop is a tax-free upstream Sec. 368(a)(1)(C) reorganization of a subsidiary’s assets (an upstream C), followed by a tax-free contribution of some of the subsidiary’s assets to a new corporation (a drop). The assets not reincorporated are left in the parent corporation’s hands.

What are the seven types of corporate reorganizations?

- Type A: Mergers and Consolidations. …

- Type B: Acquisition (Target Corporation Subsidiary) …

- Type C: Acquisition (Target Corporation Liquidation) …

- Type D: Transfer. …

- Type E: Recapitalization. …

- Type F: Identity Change. …

- Type G: Transfer.

Who must file Form 8806?

A reporting corporation must file Form 8806 to report an acquisition of control or a substantial change in the capital structure of a domestic corporation. The reporting corporation or any shareholder is required to recognize gain (if any) under section 367(a) and the related regulations as a result of the transaction.

How does a corporate reorganization work?

Corporate reorganization usually involves significant changes to a company’s equity base, such as: Conversion of outstanding shares to common stock. Reverse splits. The combination of the company’s shares that are outstanding to reduce the number of available shares.

Is reverse merger taxable?

A reverse triangular merger, like direct mergers and forward triangular mergers, may be either taxable or nontaxable, depending on how they are executed and other complex factors set forth in Section 368 of the Internal Revenue Code.

What are the 3 types of mergers?

The three main types of mergers are horizontal, vertical, and conglomerate. In a horizontal merger, companies at the same stage in the same industry merge to reduce costs, expand product offerings, or reduce competition. Many of the largest mergers are horizontal mergers to achieve economies of scale.

What is a subsidiary merger?

A subsidiary merger is a type of merger that occurs when the acquiring company uses its subsidiary company to acquire a target company. The acquirer may create a subsidiary company or use one of its existing subsidiary companies to execute the merger and acquisition transaction.

What is mergers and acquisitions tax?

Mergers and demergers are the preferred forms of acquisition in India. This is primarily due to a specific provision in the tax law that treats mergers and demergers as tax-neutral, both for the target company and for its shareholders, subject to the satisfaction of the prescribed conditions.

What are the problems of post merger integration?

- Lack of Pre-Planning: …

- No Formal M&A Integration Strategy: …

- Failure to Prioritize Workstreams: …

- Senior Leadership Void: …

- Weak Communication Planning: …

- Poor Synergy Program Management: …

- Inadequate Resourcing. …

- No End-State Transition.

What is a tax leakage?

Tax leakage occurs when investors in a fund are forced to suffer withholding taxes on dividends from the underlying shares at a higher rate than would have applied if they had purchased those shares directly.

How Much Do founders make in an acquisition?

The Founder will then receive 5% of the purchase price. You will take home $50 million in proceeds before taxes. In terms of the cash equity mix it will depend on the deal terms, your personal tax preferences, and how motivated the acquirers are trying to keep you.

What is the 2021 tax bracket?

The 2021 Income Tax Brackets For the 2021 tax year, there are seven federal tax brackets: 10%, 12%, 22%, 24%, 32%, 35% and 37%. Your filing status and taxable income (such as your wages) will determine what bracket you’re in.