Why is refinancing a loan bad

Overall, refinancing personal loans may lead to a minor drop in your credit scores due to the hard inquiries from the applications and opening of a new credit account. Over time, your scores may recover and then increase if you continually make on-time payments on your new loan.

Can I renegotiate my personal loan?

Yes. If you find that you’re having trouble making payments on your loan, your lender may consider renegotiating your personal loan terms to give you a better deal, especially if you’re in good standing with them.

Does credit score go down after refinance?

Whenever you refinance a loan, your credit score will decline temporarily, not only because of the hard inquiry on your credit report, but also because you are taking on a new loan and haven’t yet proven your ability to repay it.

How many times can I refinance a personal loan?

Refinancing a personal loan isn’t always a good idea. Technically, you can refinance a personal loan as many times as you can get approved.Does refinancing make your loan longer?

Refinancing doesn’t reset the repayment term of your loan, but it does replace your current loan with a new loan. You may be able to choose from different offers for your new loan depending on your goals, including a longer or shorter repayment term.

How can I lower my personal loan rate?

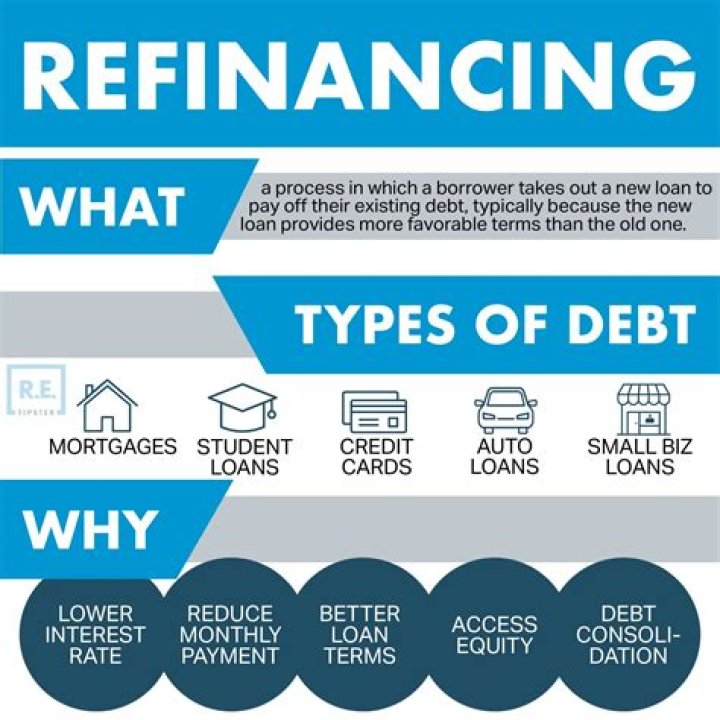

The best way to lower the interest rate on a personal loan is by refinancing the loan with another lender. When you refinance, you use a new loan or line of credit with a lower interest rate to pay off the old loan, so you owe the old balance to the new lender.

How can I lower my personal loan interest rate?

- Opt for a Higher Down Payment. …

- Choose a Loan With a Longer Repayment Tenure. …

- Go for a Step-Down EMI Plan. …

- Consider Taking Loans With Your Existing Bank. …

- Negotiate With Bank For Lower Rate. …

- Compare Before You Switch Your Lender. …

- Full or Part Prepayment Helps Reduce Loan Burden.

What does it mean to refinance a personal loan?

What does it mean to refinance a personal loan? When you refinance a personal loan, you’ll apply for a new loan — either with the same lender or a different one — and then use the funds you receive to pay off your old loan. Then you’ll begin making payments on your new loan with a new interest rate and terms.Does refinancing lower interest rate?

Refinancing can lower your monthly mortgage payment by reducing your interest rate or increasing your loan term. Refinancing also can lower your long-run interest costs through a lower mortgage rate, shorter loan term or both.

How can I get out of a high interest loan?- The Trouble With High-Interest Debt.

- Ask for a Lower Interest Rate.

- Transfer the Balance.

- Pay as Much as You Can.

- Cut Expenses.

- Wait a Few Months.

- Tackle Smaller Debts First.

- Get Credit Counseling.

Does refinancing affect taxes?

Mortgage interest and itemizing deductions Something to keep in mind is that refinancing your mortgage can significantly reduce your total tax deductions. Refinancing to a lower mortgage rate means you’ll be paying less interest, which means you’ll have less mortgage interest to deduct when tax time comes around.

How do you know if refinancing is worth it?

Mortgage rates have gone down So how much should mortgage rates fall before you consider whether refinancing is worth it? The traditional rule of thumb says to refinance if your rate is 1% to 2% below your current rate. Make sure to factor in your current loan term when considering refinance though.

How many inquiries is too many?

Six or more inquiries are considered too many and can seriously impact your credit score. If you have multiple inquiries on your credit report, some may be unauthorized and can be disputed. The fastest way to identify and dispute these errors (& boost your score) is with help from a credit expert like Credit Glory.

Why is my loan amount higher after refinancing?

Home loan interest is tipped toward the early years. … If you’ve had your loan for a while, more money is going to pay down principal. If you refinance, even at the same face amount, you start over again, initially paying more on interest. That, in effect, increases your mortgage.

Is it worth it to refinance to save $200 a month?

Generally, a refinance is worthwhile if you‘ll be in the home long enough to reach the “break-even point” — the date at which your savings outweigh the closing costs you paid to refinance your loan. For example, let’s say you’ll save $200 per month by refinancing, and your closing costs will come in around $4,000.

Should I refinance if I only have 5 years left?

The breakeven period is how long it will take you to pay off the costs of closing on a new mortgage and start realizing the savings from a lower rate and lower monthly payments. Andrews said for most people, it’s only worthwhile to refinance if your breakeven period is two years or less.

Is it cheaper to pay off a loan early?

If I pay off a personal loan early, will I pay less interest? Yes. By paying off your personal loans early you’re bringing an end to monthly payments, which means no more interest charges. Less interest equals more money saved.

What is the fastest way to pay off a high interest loan?

- Make bi-weekly payments. Instead of making monthly payments toward your loan, submit half-payments every two weeks. …

- Round up your monthly payments. …

- Make one extra payment each year. …

- Refinance. …

- Boost your income and put all extra money toward the loan.

Which bank is giving less interest for personal loan?

BankInterest Rate (p.a.)Processing FeeHDFC Bank10.5% p.a. – 21.00% p.a.Up to 2.50%Yes Bank13.99% p.a. – 16.99% p.a.Up to 2.50%Citibank9.99% p.a. – 16.49% p.a.Up to 3%Kotak Mahindra Bank10.25% and aboveUp to 2.5%

Why is my interest rate so high on my personal loan?

Personal loans have higher interest rates because they don’t require collateral. That means there’s nothing the bank can take if you fail to pay back the loan, so it charges you more in interest to compensate for the increased risk.

Can you negotiate APR on a loan?

Yes, just like the price of the vehicle, the interest rate is negotiable. … Dealers may have discretion to charge you more than the buy rate they receive from a lender, so you may be able to negotiate the interest rate the dealer quotes to you. Ask or negotiate for a loan with better terms.

What is lifetime interest on a loan?

A lifetime cap is the maximum interest rate a borrower could ever pay during the life of a loan. If interest rates exceed the lifetime cap, the borrower will still be limited to paying this maximum rate. Lenders can customize interest rate limits along with the initial, periodic, and life caps.

What percentage difference Should you refinance?

The traditional rule of thumb is that it makes financial sense to refinance if the new rate is 2 percent or more below your existing interest rate. The new rate on a refinance must provide enough savings in monthly mortgage payment to justify the cost of refinancing.

Can I refinance twice in a year?

There’s no legal limit on the number of times you can refinance your home loan. However, mortgage lenders do have a few mortgage refinance requirements that need to be met each time you apply, and there are some special considerations to note if you want a cash-out refinance.

Can I refinance for more than I owe?

A cash-out refinance replaces your existing mortgage with a new home loan for more than you owe on your house. The difference goes to you in cash and you can spend it on home improvements, debt consolidation or other financial needs. You must have equity built up in your house to use a cash-out refinance.

What is illegal interest rate?

The law says that lenders cannot charge more than 16 percent interest rate on loans. Unfortunately, some lending companies owned by or affiliated with vehicle makers have devised schemes whereby you are charged interest at rates exceeding the maximum permitted by law. This is called usury.

How can I pay off my 30 year mortgage in 15 years?

- Adding a set amount each month to the payment.

- Making one extra monthly payment each year.

- Changing the loan from 30 years to 15 years.

- Making the loan a bi-weekly loan, meaning payments are made every two weeks instead of monthly.

Is 72 month car loan bad?

Generally, yes, a 72 month car loan is bad. When you get a 72 month car loan, you’re more likely to go upside down on your car loan, which leaves you in a vulnerable financial position. Avoid getting a 72 month car loan if you can. This might mean getting a cheaper car than you hoped for.

Can I deduct closing costs on a refinance?

You can only deduct closing costs for a mortgage refinance if the costs are considered mortgage interest or real estate taxes. You closing costs are not tax deductible if they are fees for services, like title insurance and appraisals.

Can I refinance if I owe the IRS?

If there is a federal tax lien on your home, you must satisfy the lien before you can sell or refinance your home. … Taxpayers or lenders also can ask that a federal tax lien be made secondary to the lending institution’s lien to allow for the refinancing or restructuring of a mortgage.

Is a cash-out refinance considered income?

The IRS doesn’t view the money you take from a cash-out refinance as income – instead, it’s considered an additional loan. You don’t need to include the cash from your refinance as income when you file your taxes.